Understanding the Hydrogen Value Chain

Read Time: 5 Minutes

The global hydrogen market is experiencing significant change, as green carbon is introduced to a market long dominated by high-carbon hydrogen for industrial applications. Predictions for green hydrogen growth are astronomical. Just how much growth depends on whom you ask. I believe there’s not going to be as much growth as others have predicted, but I see >50% CAGR. That rapid growth is expected to occur as customers and shareholders pressure companies to lower their carbon footprints, clean air zones are introduced into cities, and companies consuming large volumes of high-carbon hydrogen consider the possibility of countries decommissioning their natural gas networks.

There are two sources of hydrogen in the hydrogen value chain: high-carbon or low-carbon hydrogen. Currently, ~99.9% of all hydrogen produced annually is high-carbon hydrogen for the industrial sector. It is a well-established market, totaling ~77 million tons a year, using this hydrogen primarily for the refining and ammonia industries. In the medium term, a new market for green hydrogen for transport is developing, and long term there may be other applications, such as the hydrogen gas grid.

The Colours of Hydrogen

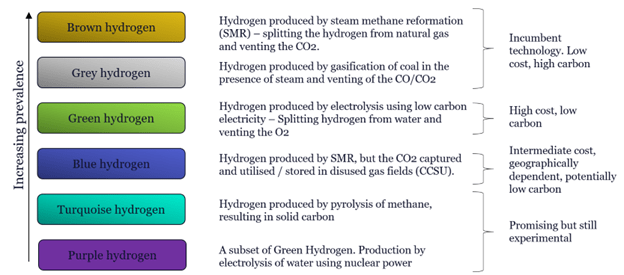

The hydrogen market is split into different colours, based on the method of production. Brown hydrogen is the most prevalent hydrogen globally. Simply put: take the methane from natural gas and put it through a reaction called steam methane reformation (SMR), which splits hydrogen from natural gas. Carbon is released as carbon oxide and vented into the environment.

Another option is gray hydrogen, made by the gasification of coal. Take coal, heat it in the presence of water, and you get a stream of hydrogen and a separate stream of carbon dioxide and carbon monoxide. It’s low cost but carbon intensive.

Green hydrogen is what most people think of as low-carbon hydrogen, and it is produced by electrolysis. Take low-carbon electricity, put it into an electrolyser, and split the water into hydrogen and oxygen. Vent the oxygen and use the hydrogen. The downside is cost, which is roughly two to four times as much as high-carbon hydrogen. It should be noted that the majority of hydrogen cost (70% to 80%) depends on electricity prices; to produce low-cost hydrogen, you need low-cost electricity.

Turquoise and purple hydrogen aren’t widely used, but turquoise in particular shows promise for the future; rather than releasing carbon as carbon dioxide, it forms solid carbon powder. In theory, you can capture that powder and bury it or convert it in another process. Because it’s a solid, it doesn’t directly enter the atmosphere.

Purple hydrogen is a subset of green. With purple, you’re splitting off hydrogen from water, but electricity comes from nuclear power rather than a renewable source, such as wind.

Blue hydrogen is interesting. It’s seen by many governments as the answer to lowering their carbon emissions at a low cost. It’s essentially the same as brown hydrogen, but rather than venting the carbon dioxide, it’s captured and used in an industrial process or pumped underground and stored in disused gas fields. Considering costs, you’re taking SMR hydrogen (at about $2/kg) and adding another process (about $1.50/kg), so it’s going to be more expensive than brown or gray hydrogen, but cheaper than green, which for most applications starts at ~$6/kg. The problem is it’s geographically dependent. Not every country can do this, because disused gas fields aren’t widely available. For those countries where it is an option, there has been a significant amount of government funding and economic investment. Blue hydrogen is popular with oil and gas companies because it fits their business model as they can still keep producing natural gas.

Worldwide, there are a handful of blue hydrogen projects operating at scale, but there are continuing questions about methane leaks and whether carbon dioxide remains sequestered. There’s no doubt blue hydrogen will be a major part of future energy processes, but there are many unknowns.

A Look at Green Hydrogen

Green hydrogen is my background. The process is simple. You start with renewable energy and power an electrolyser, which splits water into hydrogen and oxygen. You often then feed the hydrogen into low-pressure storage, and then into a compressor, because most applications for hydrogen require greater pressure than electrolysers can produce.

There are several electrolyser technologies.

- Liquid alkaline technology, the lowest cost, was commercialized around the 1930s and used at massive scale in the ’50s and ’60s. It has a large footprint and doesn’t respond quickly to changing power from, say, a solar panel. However, most industrial applications require an input of hundreds of MW, and at this scale renewable power sources change slow enough for the alkaline electrolysers to be an option.

- PEM technology was developed for military and space applications and has been commercialized over the last decade. It has a smaller footprint and responds quickly to changing power, but it’s costly and difficult to scale.

- Solid oxide electrolysis is still at the prototype stage. Its strength is its high efficiency, a consequence of running at high temperatures. But it’s costly and uses expensive, rare materials. Significant scale-up is required, but in 10 to 15 years, solid oxide technology may be used for industrial applications or centralized production.

- Alkaline exchange membrane electrolysis has been in development the last few years and has some potential. It’s not at a commercial scale yet, but it may be so in another 10 years.

People often ask which technology is “the best,” but each has strengths and weaknesses, leading them to be more suited to different applications and customers.

Electrolyser Manufacturers

Investment in these companies is significant and share prices have skyrocketed. The top-tier companies are split between big multinationals and smaller pure-play hydrogen.

What differentiates top-tier companies is the quality of their partnerships and how many different electrolyser technologies they offer. If a company marketed PEM, alkaline, and solid oxide (which presently none of them are), they could sell the best technology for a customer’s application rather than shoehorning one technology into every customer’s requirements.

Partnerships, particularly with EPCs, are crucial. Each of the top-tier companies has partnered with an EPC: Linde Engineering is partnering with ITM Power; Nel has partnered with Wood; and Siemens has an in-house EPC, as do Thyssenkrupp and Cummins.

In summary, the markets for hydrogen are growing rapidly, and there are many opportunities for to enter these markets, either directly or as a supplier or subcontractor.

About Dr. Kris Hyde

Dr. Kris Hyde is a leading U.K. authority on hydrogen technologies and the hydrogen market and has 18 years of experience in this space. He was recently a senior manager at ITM Power Plc, where he worked in the key teams of Science, Engineering, and Commercial, giving him a broad understanding of hydrogen technologies. He is currently a director of consulting firm HYDErogen, Director at Hollingworth Design Limited, and a consultant to the European Marine Energy Centre (EMEC) Ltd. and ZEMtech.

This energy industry article was adapted from the GLG Webcast “Understanding Hydrogen Value Chain.” If you would like access to events like this or would like to speak with technology industry experts like Dr Kris Hyde, or any of our approximately 1 million industry experts, please contact us.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。