The Russia-Ukraine War and Its Impact on Global Agriculture

Read Time: 4 Minutes

With access to GLG’s Library, you can watch this webcast on-demand.

The economic impact of the Russia-Ukraine conflict largely has been felt in the energy area, with Europe struggling to find substitutes for Russian oil and natural gas. But the conflict also has affected global agriculture markets, perhaps most directly in the areas of wheat, corn, sunflower oil, and fertilizer. The following is an overview of the war’s effect on those markets and where things may be going.

Wheat Production

According to the U.S. Department of Agriculture’s monthly World Agricultural Supply and Demand Estimates report (WASDE), global wheat production stood at about 775 million tons in 2021, with 110 million tons, or about 14%, accounted for by Russia and Ukraine. That’s a meaningful share, but there are many players of comparable scale, including China and India, which are big producers for their own domestic consumption. Russia and Ukraine, however, accounted for about one-quarter of the 200 million tons of wheat that got traded internationally last year, ranking with other large producers and exporters, including the U.S., Argentina, and Australia.

Corn Production

In corn — the largest grain globally in terms of production at 1.1 billion tons — Russia and Ukraine represent only about 4% of global production but about 15% of global trade, with most of that coming from Ukraine.

Sunflower Oil Production

Although Russia and Ukraine account for a major portion of the world’s production, sunflower oil represents a relatively small share of the total global picture for edible oils. Of the 206 billion tons of global edible oil production in 2021, sunflower oil accounted for only about 19 million tons, or less than 10%. Russia and Ukraine accounted for a meaningful 11 million of those tons, so they are clearly the leaders in sunflower oil, which can best be described as a niche regional market centered on Russia, Ukraine, Turkey, and the European Union.

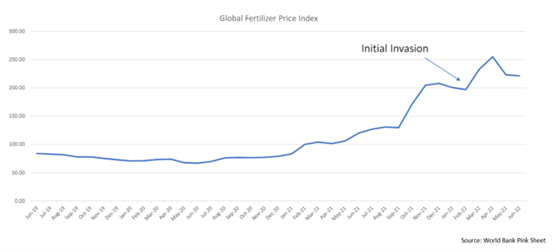

Fertilizer Production

Compared with markets for wheat, corn, and sunflower oil, the fertilizer market is probably the most complex of all. With fertilizer, we’re really talking about its key components: nitrogen, phosphorus, and potassium. Nitrogen, the most significant component, is manufactured largely from natural gas and produced in a solid form known as urea or as a liquid known as anhydrous ammonia. Phosphorus and potassium are mined. They are mixed in different proportions depending on the agricultural application.

When looking at the three components collectively, China is the leading global producer by tonnage, with Russia a strong second overall due to its second-place position behind Canada in the potash market, which is the major source of potassium, and its fourth- and fifth-place positions, respectively, in nitrogen and phosphorus. In terms of exports, the picture is diverse and fragmented, given the complexity of manufacturing and sometimes mixing and compounding in many locations. Overall, however, Russia accounts for about 15% of fertilizer exports.

Based on their share of world markets in these commodities, the Russia-Ukraine conflict has resulted in more of a dislocation of supplies rather than their destruction. In mid-July, the USDA estimated combined Russian and Ukraine wheat and corn production to be unchanged from its January estimate. Looking at export trade flows, however, July estimates for wheat exports from Russia and Ukraine were down 7 million tons from January estimates, while corn export estimates were down 10 million tons for the two countries.

Reactions to Russia/Ukraine Shortages

Much of the response to dislocations in supply involves substitutions. With sunflower oil in shorter supply, for example, there has been a switch to palm oil and soybean oil. In fertilizer, Canada has been a good alternative to Russia; Canadian fertilizer exports to Brazil, for example, jumped 70% in the first six months of 2022.

Overall, agricultural markets have responded to the crisis rationally. Wheat prices, for example, spiked shortly after the start of the war and then moderated and returned to pre-invasion levels and sometimes even below. Corn has been similar, with U.S. fundamentals being a much bigger driver of price movements than anything happening in Russia and Ukraine. While corn was expected to be a big export for Ukraine in 2022 and 2023, the shortfall due to the war will be felt in Ukraine but won’t have much of an impact on world supplies or prices.

Unlike grain prices, however, fertilizer prices are likely to remain high since natural gas is a major raw material in its production and its price. Fertilizer accounts for between 20% and 35% of agricultural production costs at the farm level, so future price shocks in natural gas could have a significant effect on agricultural supplies and prices.

The main takeaway, however, is that the global agricultural system is robust and flexible, with price signals doing a good job of bringing together supply and demand in a way that bridges short-term crises. Long term, Russia and Ukraine will maintain their role in the system, with each side seeing that reaching some mutually acceptable workarounds, at least in the agricultural area, is in their own best interests.

About Doug Christie

President of Cargill Cotton from June 2009 to March 2016, Doug Christie is now an independent commodity trader and consultant. In addition to heading Cargill’s global cotton trading business, he served in several management and executive roles in the company’s grain, oilseeds, and biofuels businesses and has worked extensively across the U.S., Canada, and in four Asian locations during his career.

This agriculture industry article was adapted from the GLG Webcast “Crops, Agriculture, and Biofuels — Impact of Russia-Ukraine Conflict.” If you would like access to events like this or would like to speak with agriculture industry experts like Doug Christie or any of our approximately 1 million industry experts, please contact us.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。