Survey: UK High Street Christmas Retail and 2021 Predictions

Read Time: 5 Minutes

Hundreds of stores closed on UK’s High Street last year due to COVID-19. How did this affect holiday sales and retailer predictions for 2021 and beyond?

To find out, GLG conducted an online survey to assess 2020 Christmas retail sales outcomes by channel (online versus in-store), product category performances, overall confidence levels in year-over-year (YoY) retail sales, and the impact of initiatives like “click and collect,” where shoppers purchase items online and then pick them up at the store.

The results provided surprising insights into retailers’ 2021 predictions and beyond.

About the Survey

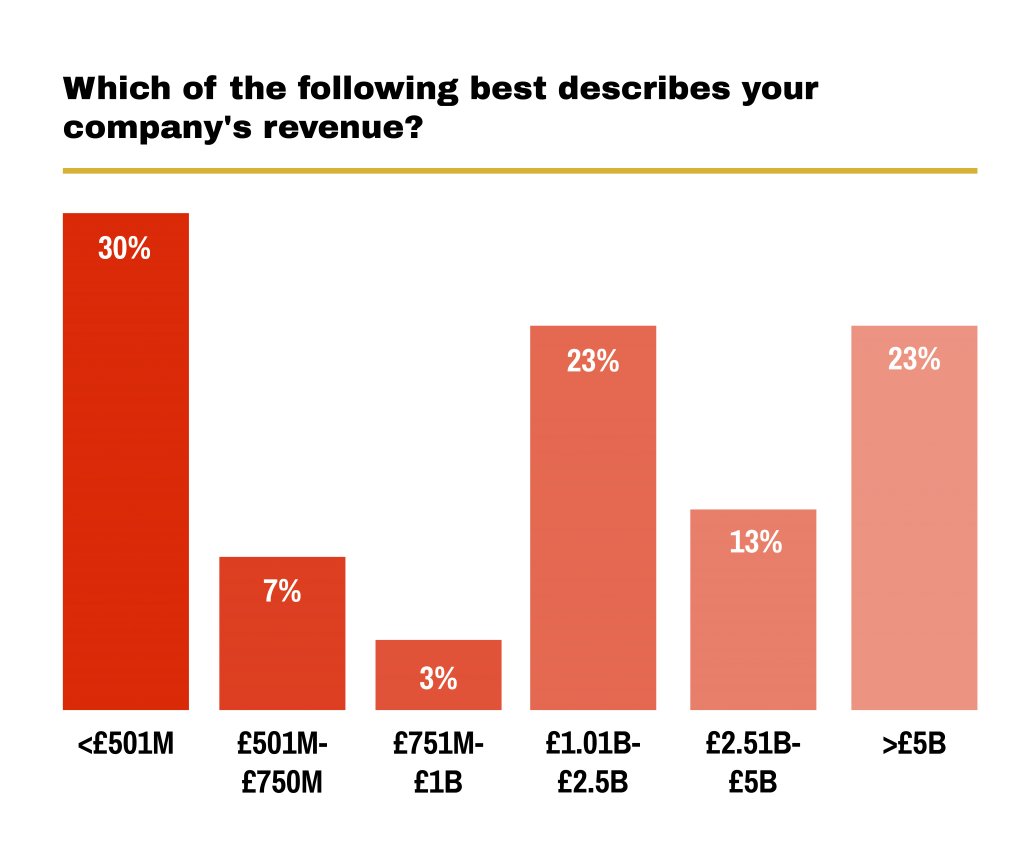

From December 23, 2020, until January 8, 2021, GLG sought responses from top retail players in the UK High Street.

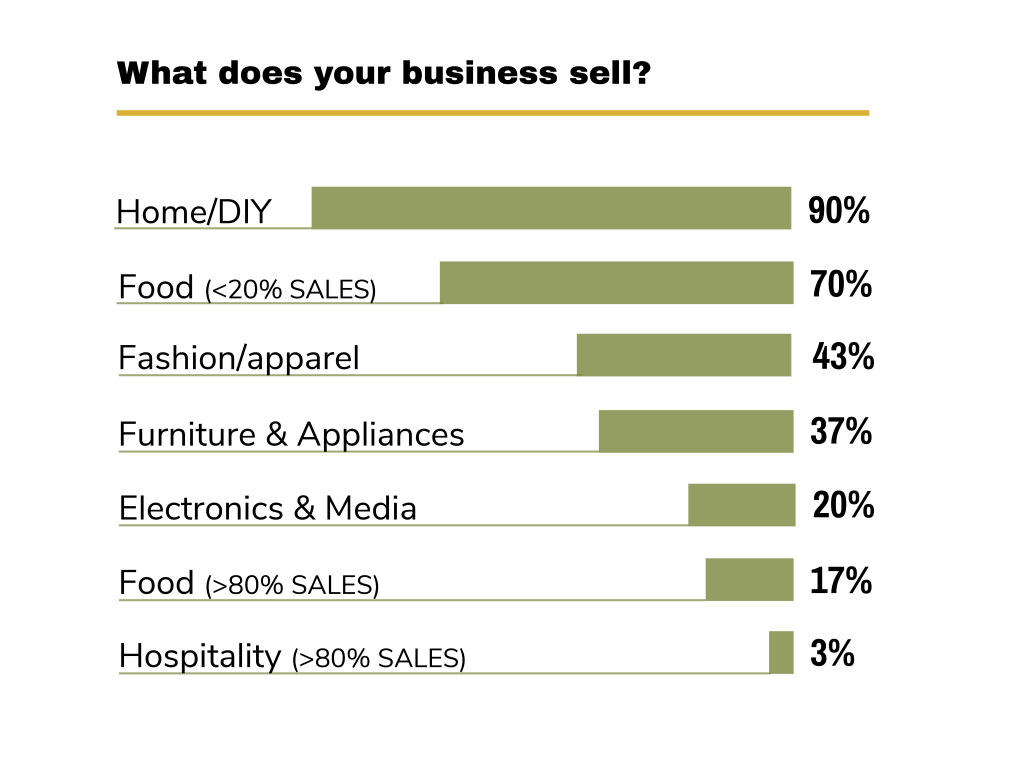

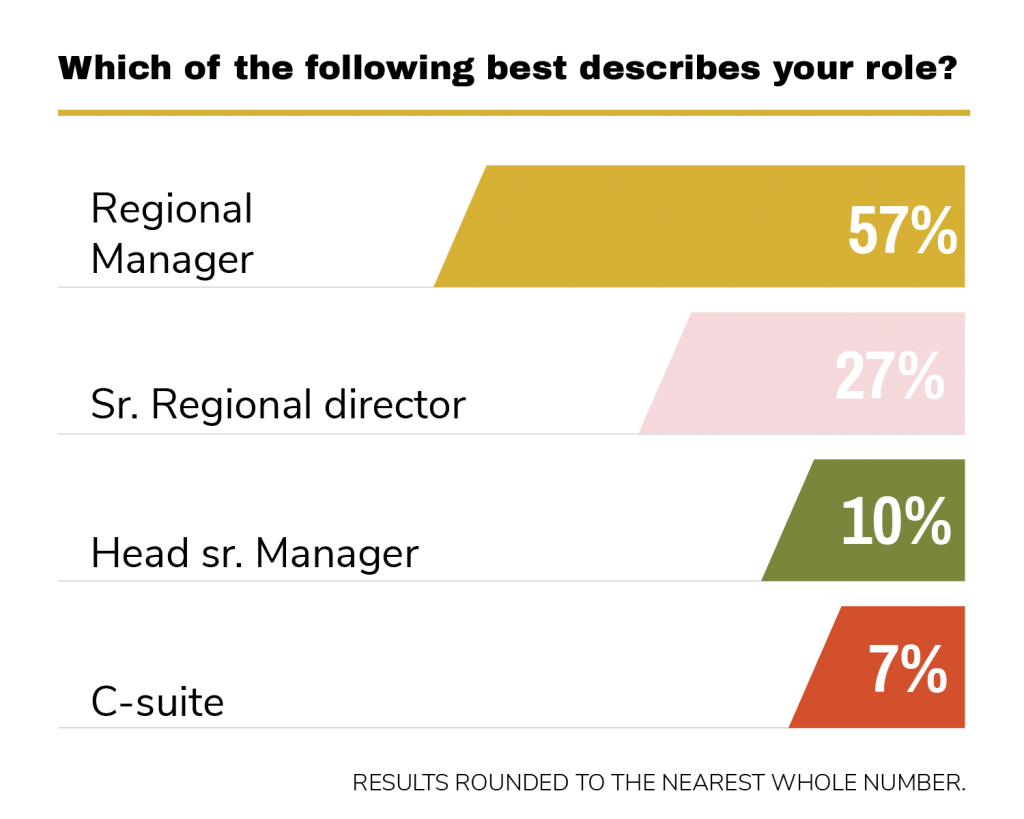

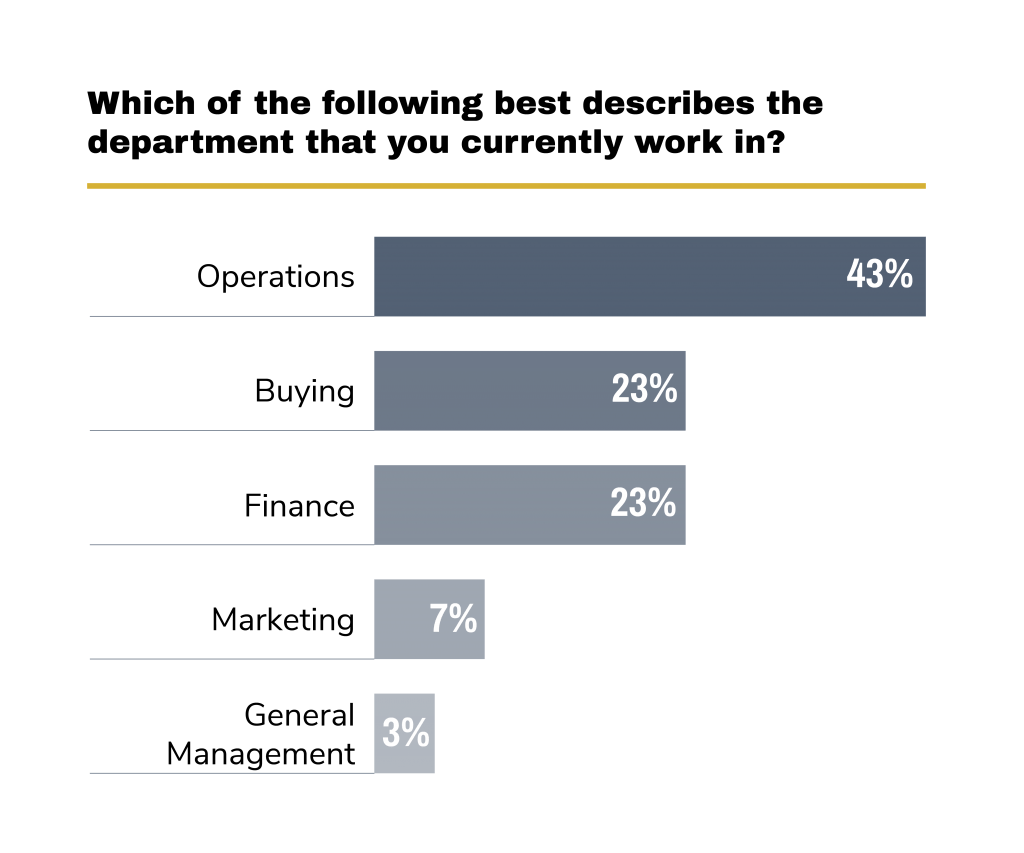

A total of 2 C-suite executives, 17 regional managers, 8 senior regional directors, and 3 head senior managers at UK companies with revenue from £251 million to over £5 billion responded in departments including operations, buying, finance, marketing, and general management. All had oversight of performance and sales volumes of their stores, with respondents representing retailers that have at least three physical stores and sell nonfood products.

Surprising Results

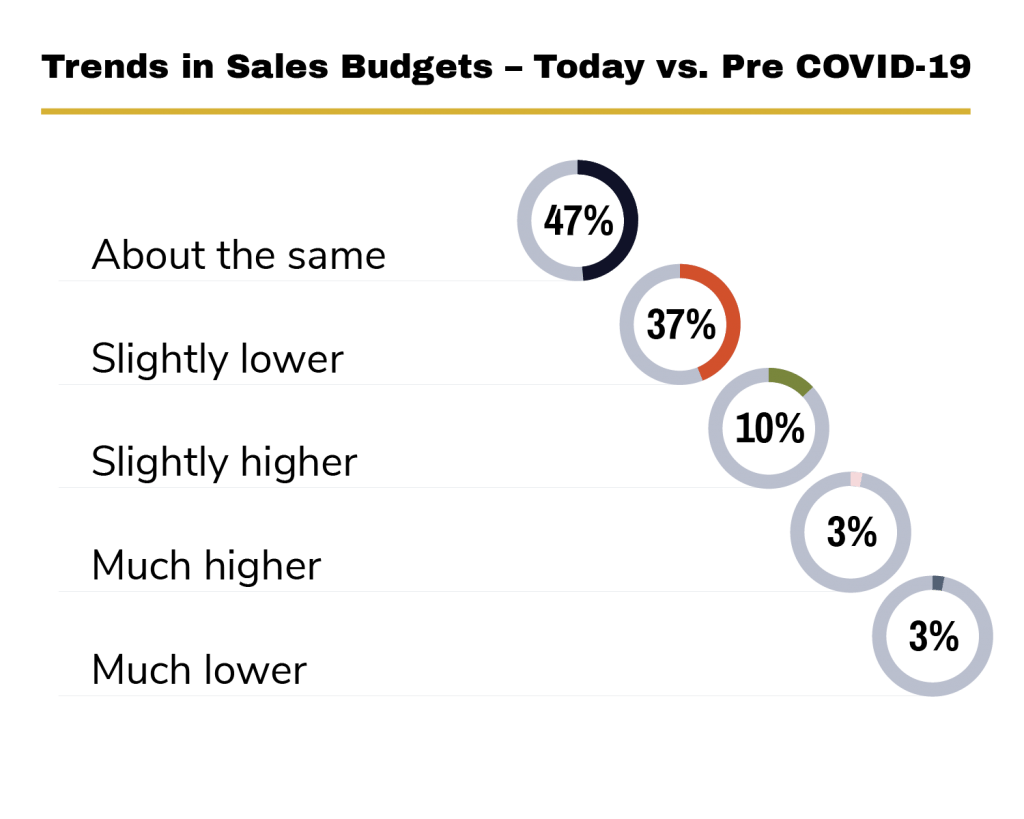

Many feared low sales during the 2020 Christmas shopping period, but the numbers were not as extreme as expected. In fact, 60% of respondents ended up meeting or exceeding their total sales budget for the year, with 37% stating they were only just “slightly lower.”

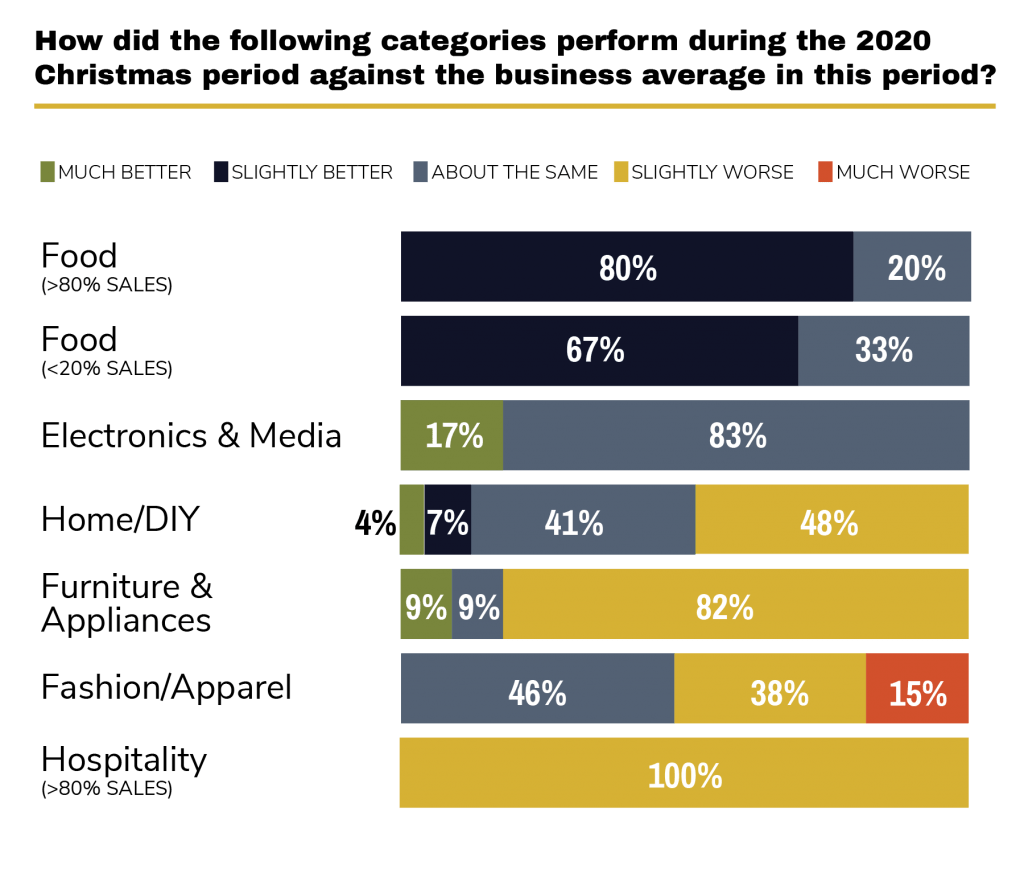

As expected with cafés and offices closed due to COVID-19, over 67% of respondents selling food indicated they did “slightly better” than last year. Likewise, with more people likely upgrading their work-at-home systems, electronics and media retailers reported sales were “much better” (17%) or “about the same” (83%). There was also a spike in home office furniture purchases.

Profitability

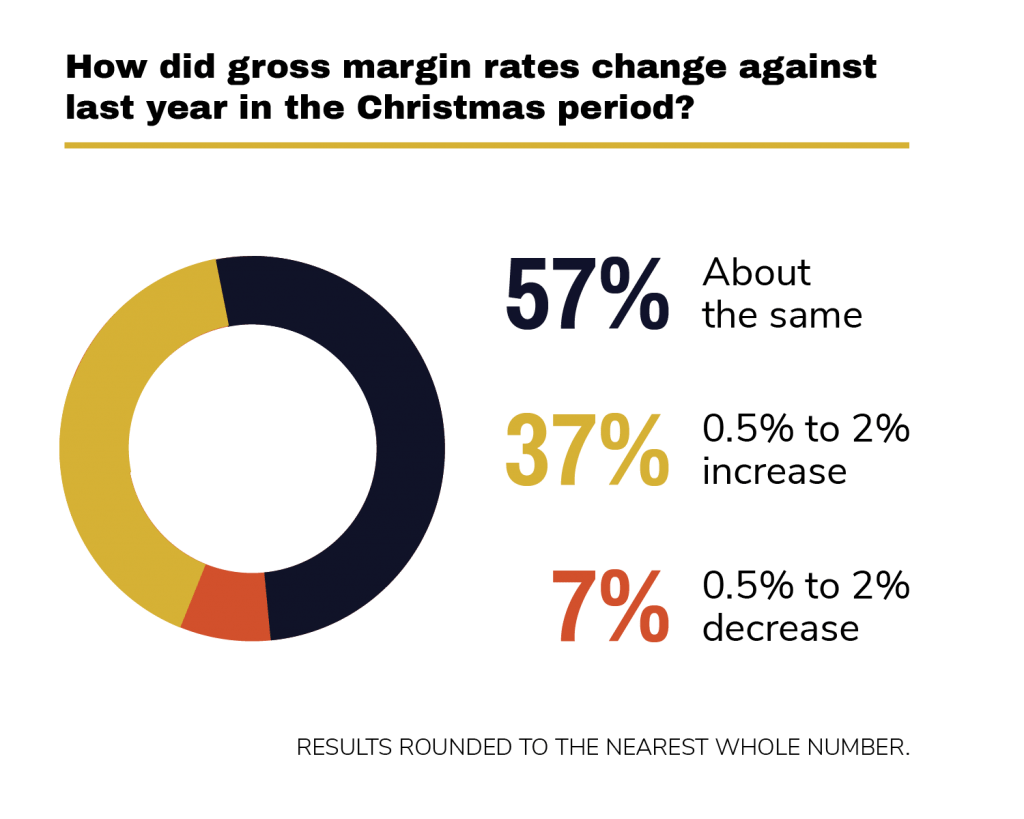

The big surprise is that respondents indicated retail profitability was relatively robust, with 37% claiming an increase in YoY gross margins.

While it may be expected during a pandemic to see retailers increase prices, offer major discounts to offload stock overloads, and decrease rents, these numbers remained balanced similar to recent years.

According to Simon Russell, former Director of Operations Development at John Lewis, this may be due to the fact that “retailers built buffers to accommodate for changes in the value of the pound [and] are holding off until travel season starts again to reduce the price of their summer stock… [They may have] made some agreement with their landlords about rent reductions.”

Channel Sales

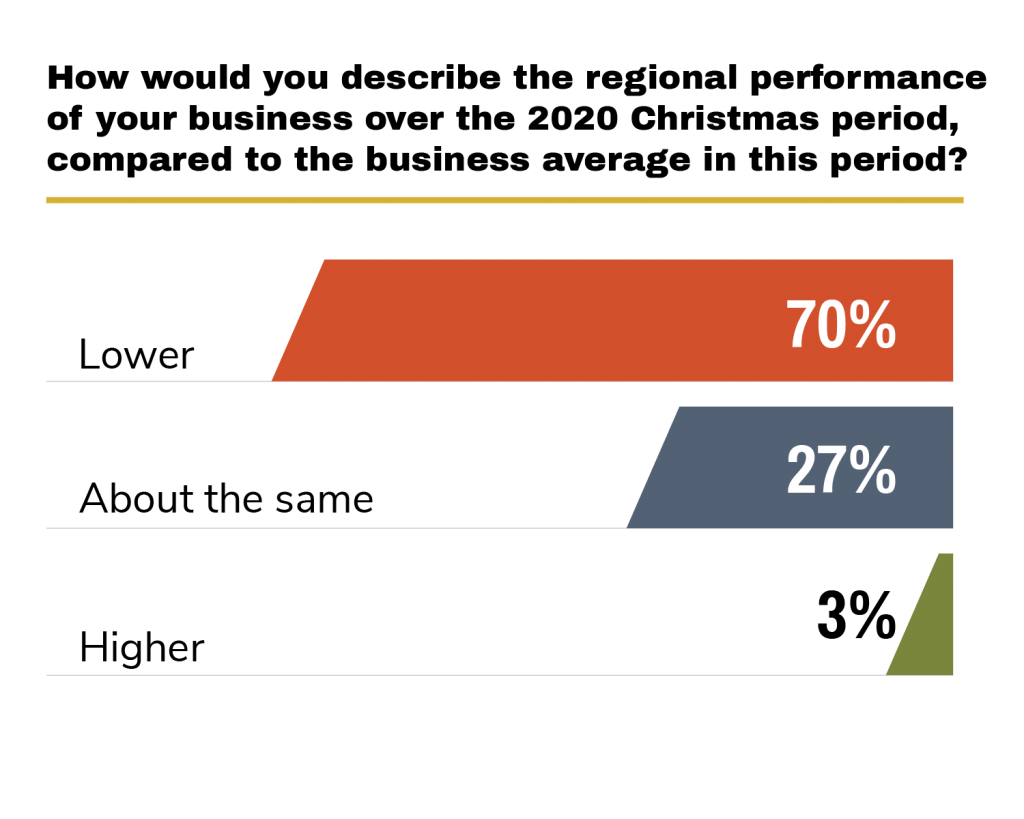

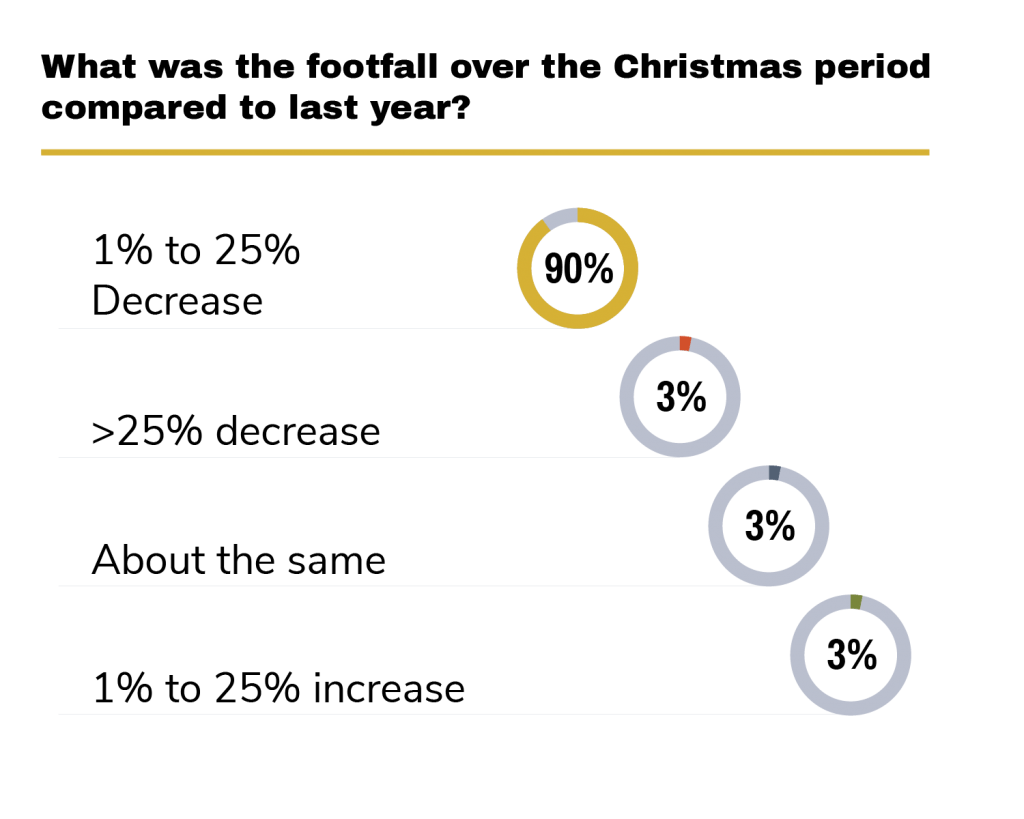

Looking in more detail at brick-and-mortar versus online sales, the number of people who actually visited the shops, or footfall, was predictably lower. Specifically, 90% of respondents saw a 1% to 25% decrease in 2020. This impacted the southwest, southeast, and Northern Ireland regions most, and YoY in-store sales trends were 70% lower overall.

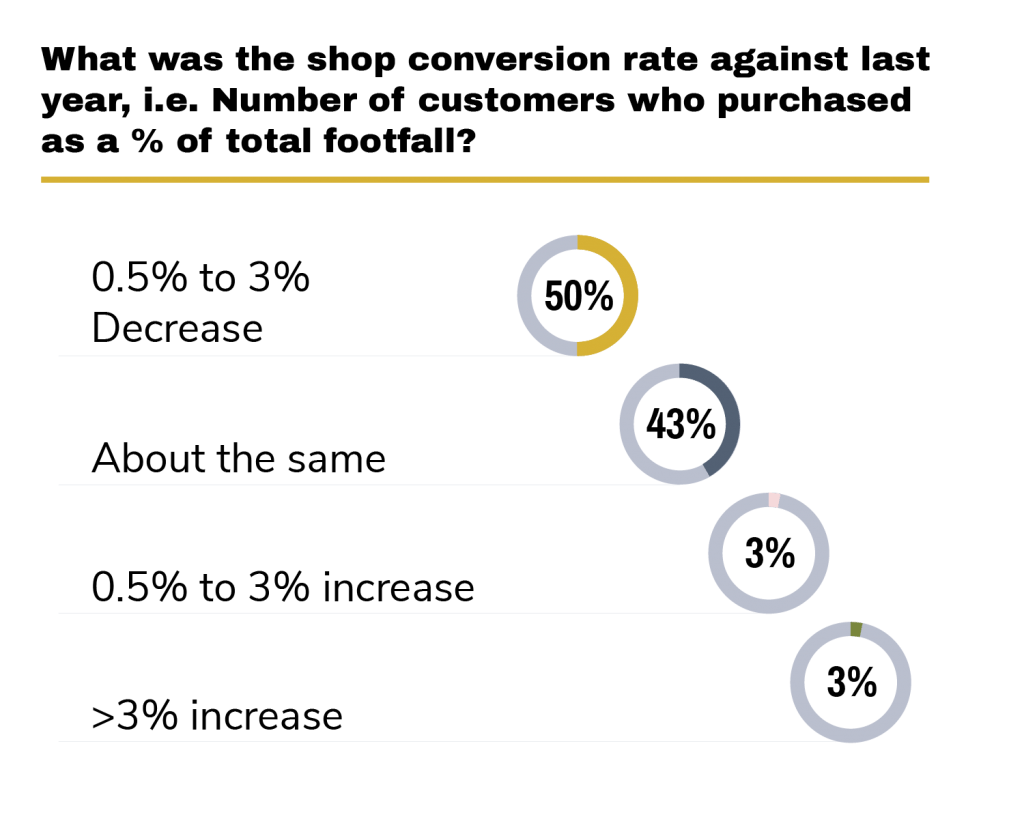

However, this is potentially better than expected, especially with footfall purchases staying roughly the same at 43%, with about 50% reporting a declined conversion rate.

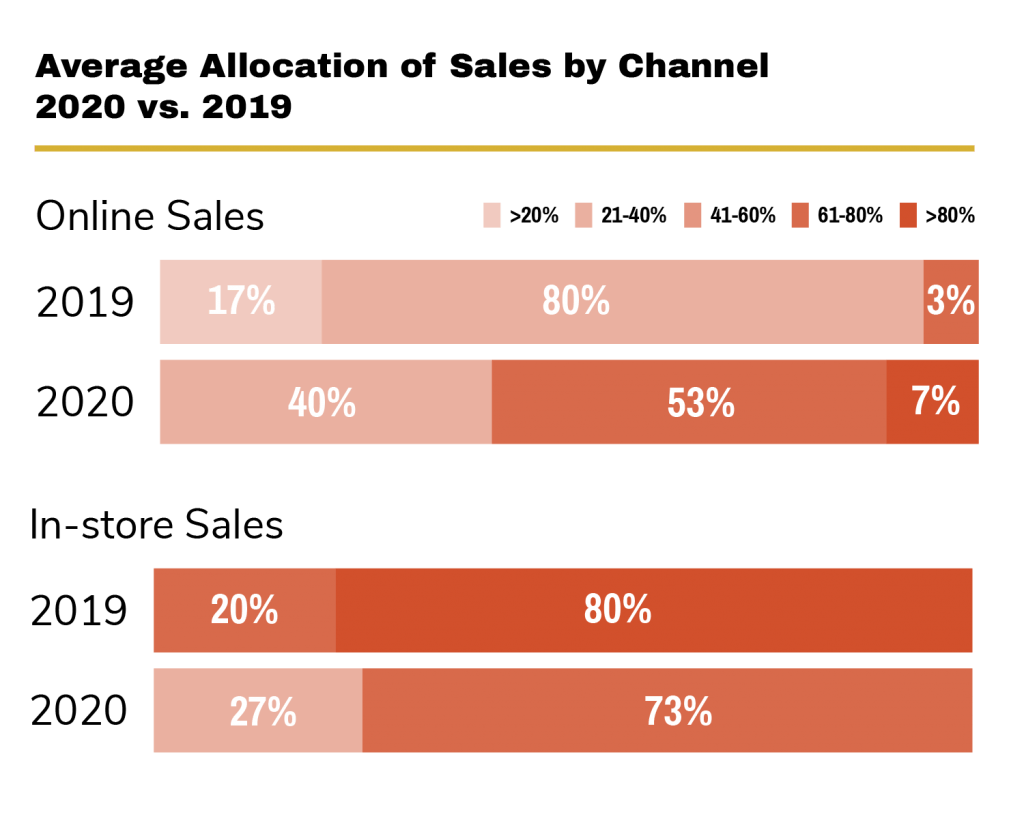

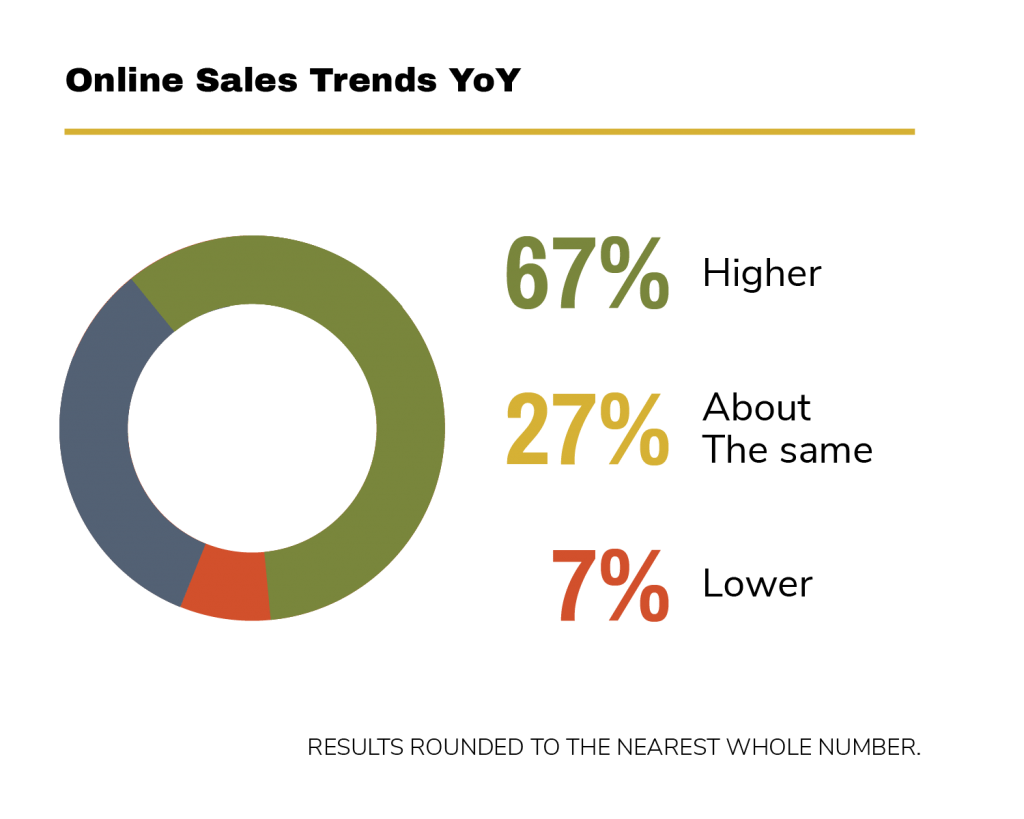

As in-store sales declined, unsurprisingly, YoY online sales trends increased. Respondents indicated they were higher (67%) or about the same (27%) as 2019 levels, with 70% reporting they roughly matched 2020 in-store sales.

But it’s important to note that these numbers included click and collect sales, which grew in popularity over the Christmas shopping season. It was a leading fulfilment choice for about 25% of respondents, with 87% indicating that 2020 click and collect sales counted toward a mixture of in-store and online sales.

Overall, most respondents indicated that Christmas sales and profitability were better than expected without any real extremes. But what do they say about the future?

2021 Predictions

Survey results indicate positive predictions from retailers for 2021 and beyond. Specifically, 83% of respondents predict a 1% to 25% increase for overall sales this year, and only 10% anticipate a sales decline.

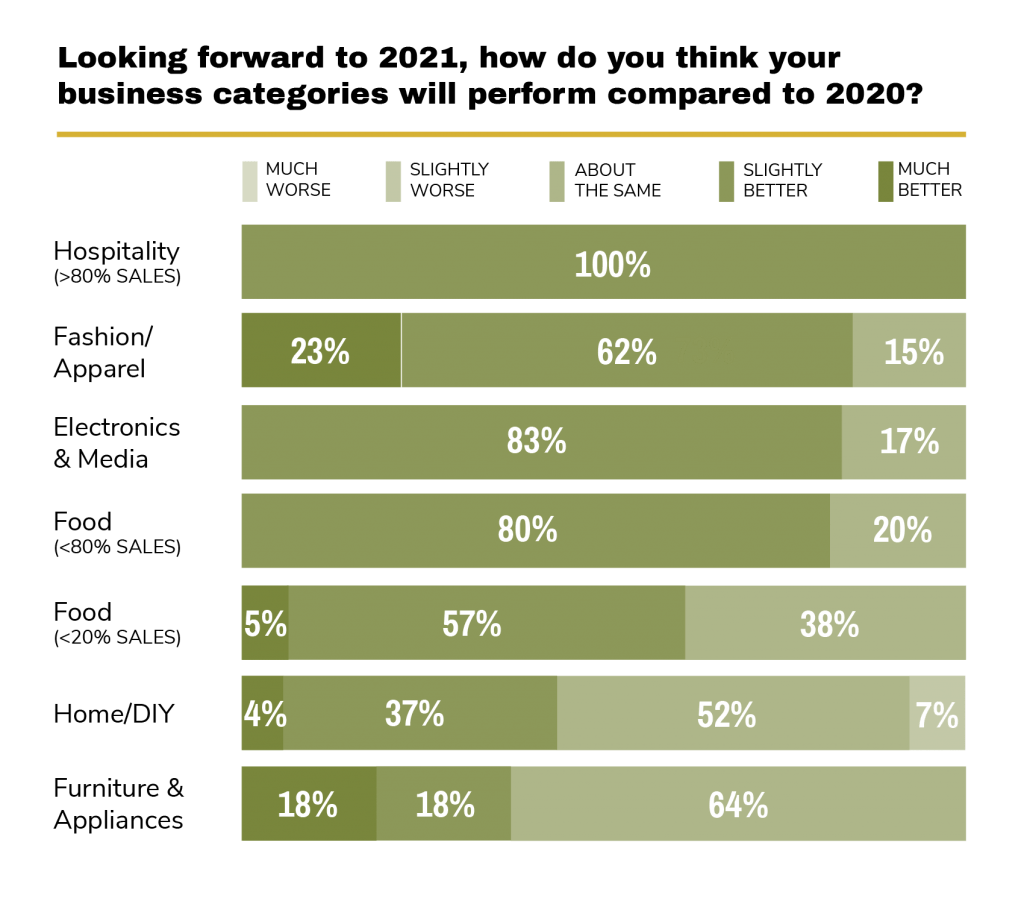

All categories (except home/DIY and furniture and appliances) expect YoY sales performance improvements.

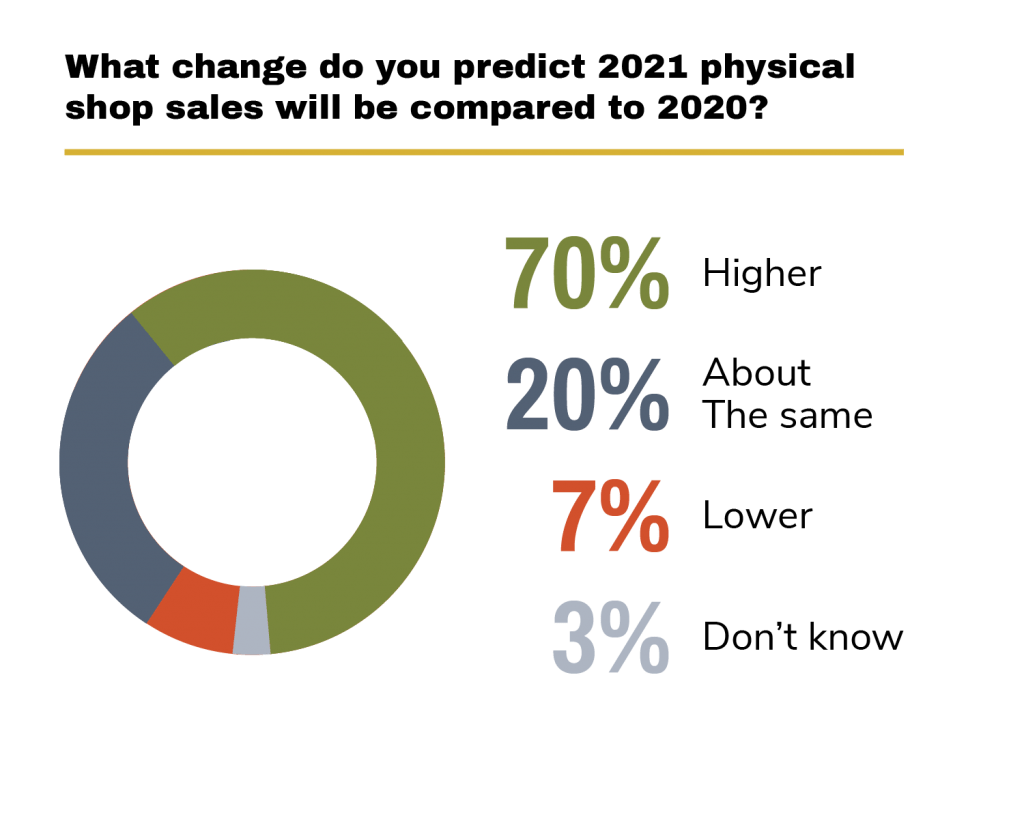

Likewise, the majority of respondents predict that online sales will continue to grow in 2021 but at a slower rate, with 73% anticipating a 1% to 25% increase. And surprisingly, 90% anticipate in-store sales will return to, or exceed, pre-COVID-19 levels, with London, the northeast, and Scotland seeing the most positive impact.

In fact, 87% of respondents expect to keep their shops and 60% plan “modest growth” to their number of physical stores of around 5% to 19% by 2023.

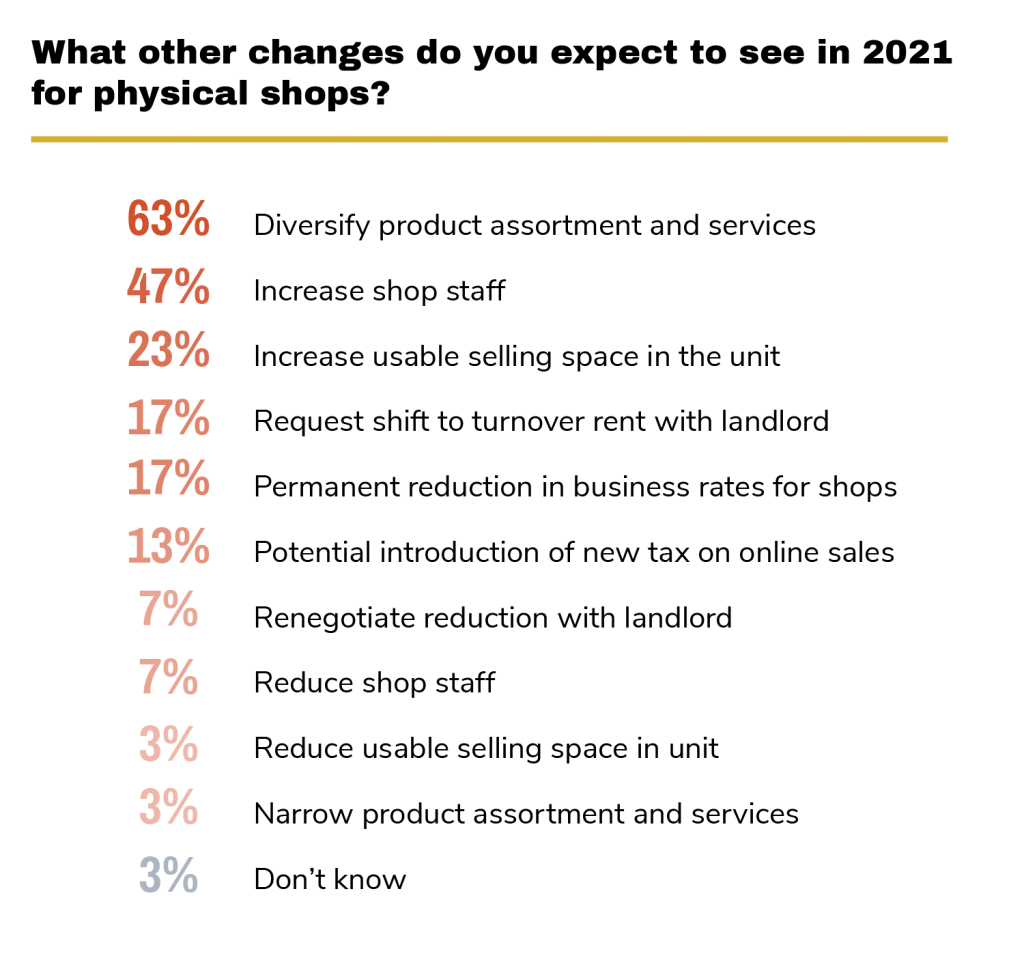

These numbers may seem optimistic, but the results indicate that retailers are making changes to offer unique customer experiences unavailable online in order to grow. Specifically, they plan to diversify their product assortment and services (63%), increase shop staff (47%) and their usable selling space in the unit (23%), request a shift to turnover rent with their landlord (17%), and more.

Summary

Lower retail sales YoY for the 2020 Christmas period were expected, but the survey results reveal that sales performance and in-store sales were much better than many anticipated. Retail prices held up strong with normal levels of discounting, and click and collect volumes grew sharply.

Plus, retailers are optimistic about 2021 sales performances, with expected growth to be about the same or exceeding 2019 levels. Confidence is up, as the majority predict online sales will continue to grow (albeit at a slower rate than 2020) and in-store sales will increase sharply in 2021 as COVID-19 restrictions lift.

With more travel and events, most expect the hospitality and fashion/apparel categories to bounce back significantly and to maintain current shop numbers throughout 2021. Many respondents even expect to increase their physical shop locations by 2023.

But for this growth to occur, respondents feel it’s crucial that retailers fix pain points in the omnichannel customer experience. When brick-and-mortar shops update their spaces to offer customer experiences unavailable online, and predicted tax and rate changes begin, there will be a level playing field for shops versus online sales, likely saving the High Street.

If you need insights from a hard-to-reach niche audience, contact GLG to learn more about its new Network Surveys.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。