Survey: The Post-COVID Future of Private Higher Education

Read Time: 3 Minutes

The private higher education space is known to global investors as having the potential for high operating margins, and it has seen significant growth in interest in recent years. COVID-19 has significantly disrupted the space, creating strong interest in the sector as regions emerge into post-pandemic economies and investors seek opportunities.

The space in both the U.S. and Europe has niche operators that have developed successful and sustainable platforms. The environment is showing signs of optimism, and there is movement toward both further consolidation and divestitures, with merger and acquisition players challenging for best positions. The disruption has also likely accelerated the change to increased online delivery, which again gives cause to look for upward changes in margin potential. Interest in the sector is high. Investors seem poised to participate in the emerging opportunities.

Survey and Panel Demographics

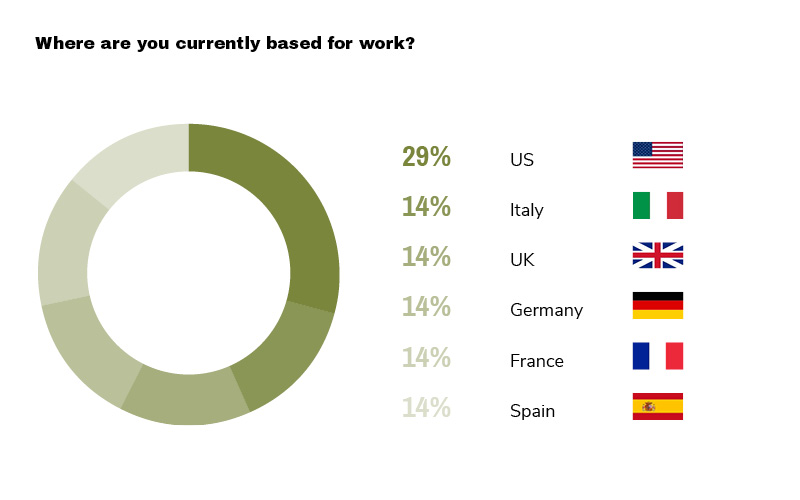

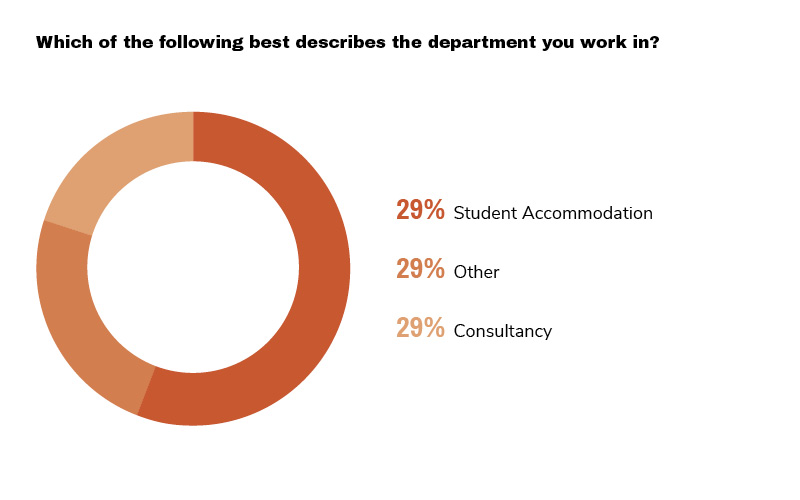

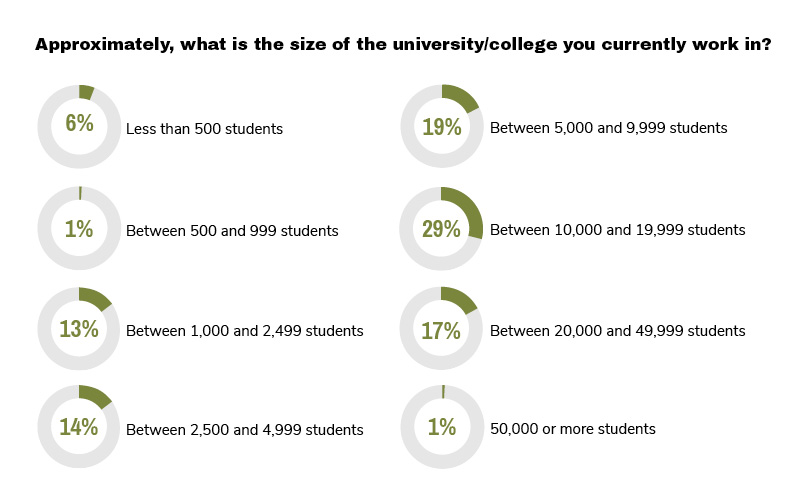

To understand the dynamics within the private higher education space during COVID-19, GLG conducted a survey between April and May 2021 of 70 professionals working across the U.S. (29%) and Europe (71%). A proportion of the experts (24%) we surveyed were members of their institution’s governing board (Dean/President), 20% were part of the administration, and the remaining 56% were part of the faculty body knowledgeable about the COVID-19 impact on their institution and able to discuss the outlook for the next several years in comparison with the public higher education space. Fifty-three percent of the respondents surveyed are currently working in institutions of less than 10,000 students, with 34% stating that more than 40% of their student base is international.

Impact of COVID on Private Institutions Expected to Be Short Term

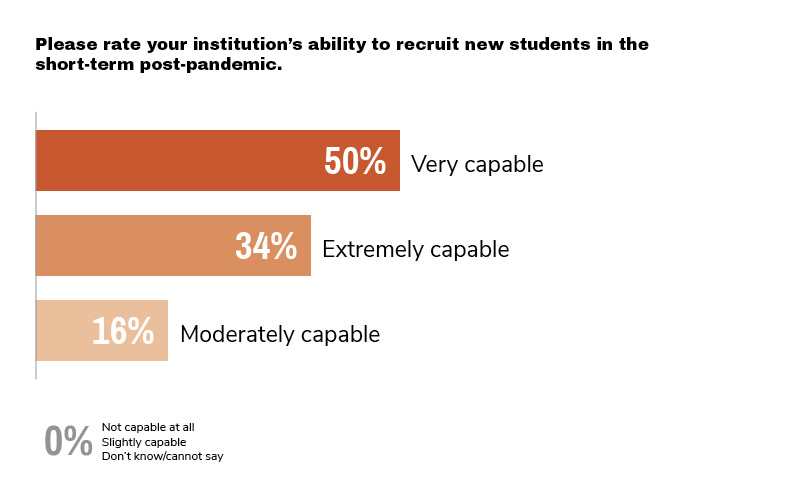

Faculty and management of private institutions see the pandemic impact to be short term and are optimistic about the resumed volumes of post-pandemic education delivery. The disruption caused educators to focus more on student communication as well as an increase in student care and innovation. All our respondents express some level of confidence in their institution’s ability to recruit new students post-pandemic, with a whopping 84% rating their capability at either “very capable” or “extremely capable.”

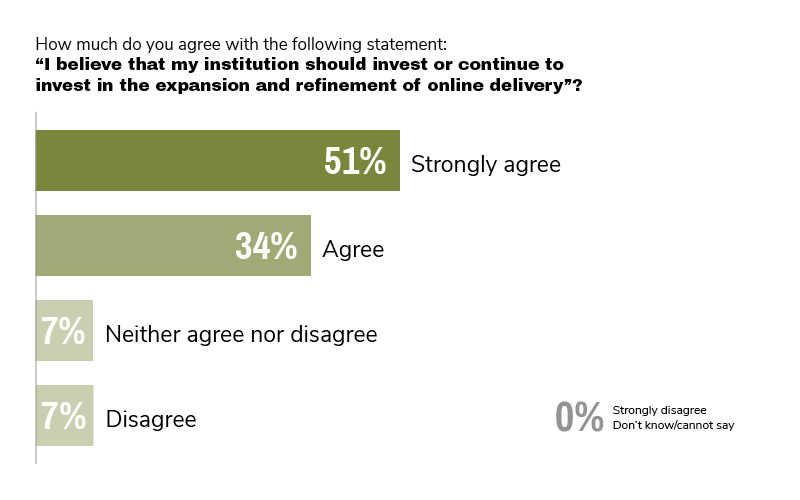

Investment in Online Higher Education Delivery

Faculty and management of private institutions are bullish on trends in online delivery, with 85% of all respondents agreeing that their institution should invest or continue to invest in the expansion and refinement of online delivery.

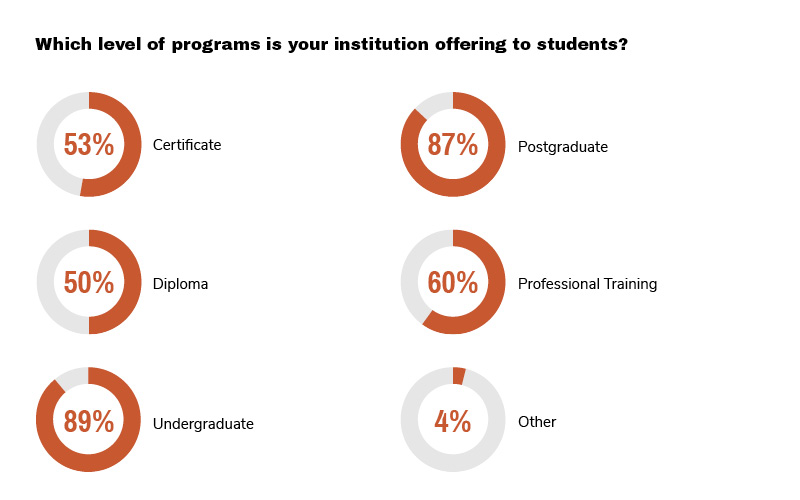

Opportunities for High Margin Courses

Faculty and management of European private institutions have the opportunity to follow the trends of U.S.-based private institutions and introduce a larger number of high-margin postgrad and professional-type courses to help increase their niche and developed brand required for sustainable growth. The survey, for example, shows that only 60% of respondents’ institutions are currently offering professional training courses.

European institutions should look to U.S. institutions for best practices in recruitment capabilities, quality of faculty, student outcome, and alumni relationships for continued growth and acquisition of market share versus public institutions.

Higher Education Tuition: Public vs. Private

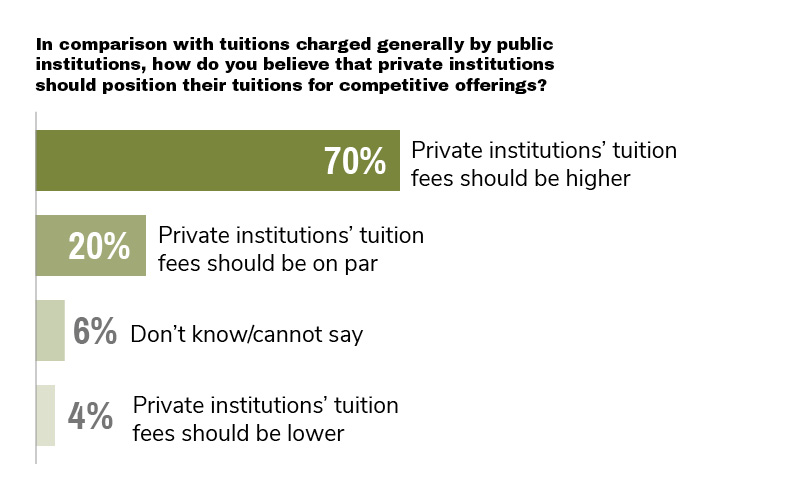

Faculty and management of private institutions understand the need to be mindful of tuition in comparison with their competitors, including public institutions, given their lack of publicly supported funding subsidies. Our survey shows that 90% of respondents believe that in comparison with the tuitions charged generally by public institutions, the tuitions at private institutions should be at par (20%) or higher (70%).

Increasing tuition to meet rising costs is seen as necessary and will create the type of sustainable margins required to secure and increase money market investment from private equity and the investment community for future market share and growth. This includes demonstrating value by brand building by focusing on improving student outcomes, better communication with students and alumni, and investing in delivery systems and faculty.

Conclusion

The private higher education sector has been seriously impacted by the COVID-19 pandemic causing global disruption to face-to-face instruction. This disruption is seen largely as twofold, with belief that the impact is short term in duration and will lead to shifts in delivery — largely to online and hybrid options, which provide opportunity for increased distribution and reach as well as the potential for increased value in operating margins.

Sample Questions Covered in the Full Private Higher Education Network Survey:

- In your view, how likely are students enrolled and active pre-pandemic to discontinue their studies?

- For any students who were able to take courses during the pandemic, please rate the support received from faculty and administration.

- How likely is a change to the community feel of student participation in post-pandemic delivery of programs (e.g., more online demand rather than face-to-face learning sessions)?

- You mentioned your institution was not offering online programs pre-COVID-19. How likely is it that your institution will include online programs in the next one to three years?

- How much do you agree with the following statement: “I believe that my Institution should invest or continue to invest in the expansion and refinement of online delivery”?

- In your view, what are the competitive advantages/disadvantages private institutions have over public institutions?

Click to Get Access to These Results

or to See Our List of Other Network Surveys

About Network Surveys

GLG’s Network Surveys administer research on market-moving topics and trends, surveying relevant subject matter experts. Each survey focuses on a specific industry, and the survey respondents have in-depth expertise about latest development in the industry. To ensure that the survey’s focus is relevant to the panelists, our Network Surveys team partners with a GLG expert with deep industry knowledge to write the questionnaire. GLG currently runs approximately 12 Network Surveys every month.

The standard deliverables for our Network Surveys include:

- 1 x individual responses (“raw data”) in Excel.

- 1 x PPT report with aggregated data.

- For selected topics: Executive summary with key takeaways and conclusion.

- For selected topics: In-depth PowerPoint report of survey findings presented by the Network Member via webcast (optional).

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。