Survey: Semiconductors Supply Chain

Read Time: 3 Minutes

In early 2020, COVID-19 took the world by surprise. The resulting lockdowns caused demand for new automobiles to collapse, which in turn drastically reduced orders for semiconductors from the auto sector. Other semiconductor sectors related to home office, high-bandwidth networking and gaming surged in demand and consumed the available semiconductor capacity. When automotive semiconductor demand stepped back up in late Q4 2020, the industry got a wake-up call and experienced unprecedented interruption in the supply chain.

Survey and Panel Demographics

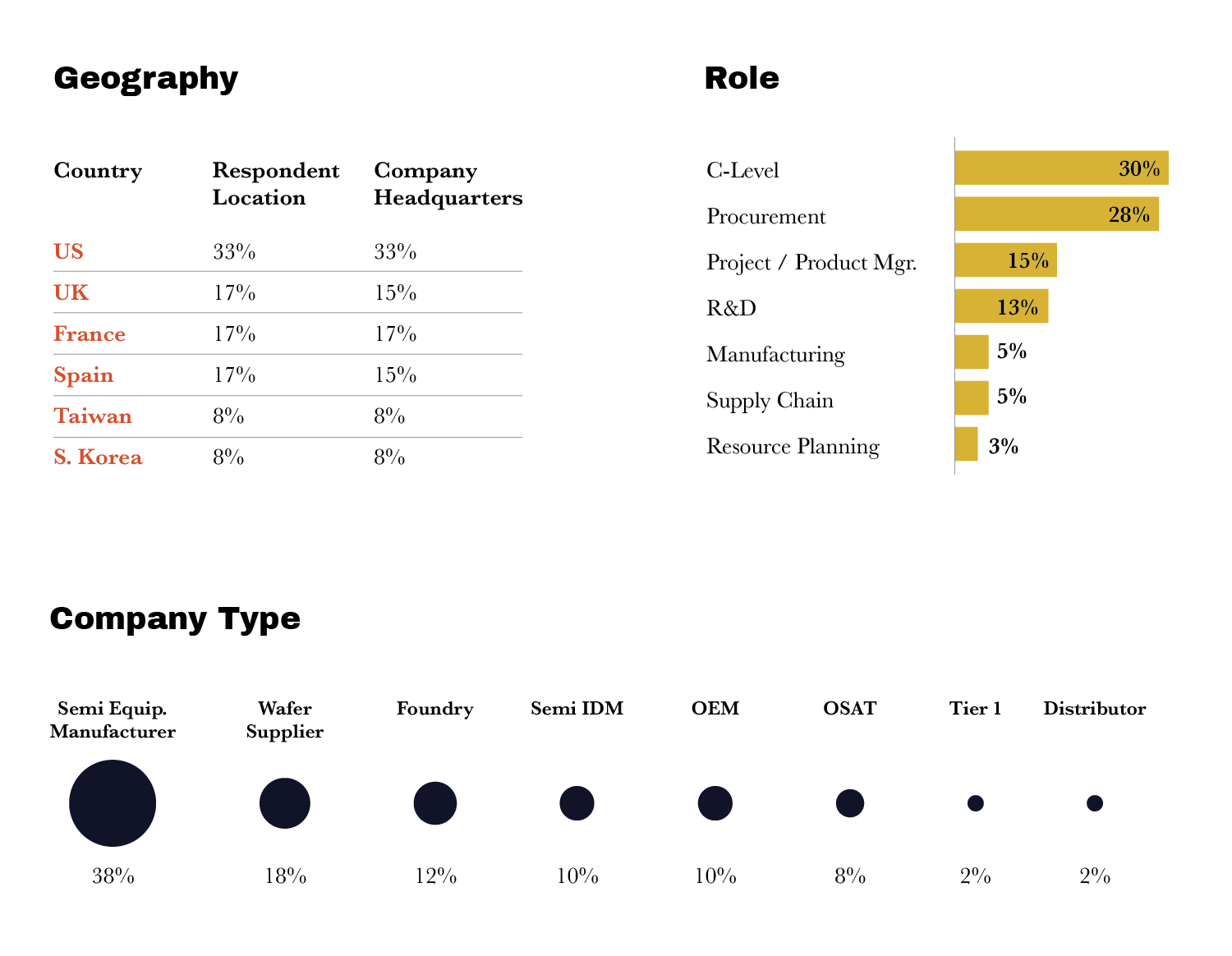

To understand more about the current market dynamics within the semiconductors supply chain space, GLG conducted a survey of 60 senior executives across the U.S. (33%), UK (17%), France (17%), Germany (17%), Taiwan (8%), and South Korea (8%). Of those surveyed, 30% were C-suite executives, 28% procurement professionals, 15% project/product managers, 13% R&D professionals, 5% manufacturing professionals, 5% supply chain professionals, and 3% resource planning professionals.

These respondents work at a variety of company types, including semiconductor equipment manufacturers (38%), wafer suppliers (18%), foundries (12%), semiconductor IDMs (10%), OEMs (10%), OSATs (8%), tier 1 (2%), and distributors (2%). All of these respondents were knowledgeable and able to discuss the strategic changes businesses are making to manage potential shortages going forward, including expectations for inventory levels.

Different Semiconductor Nodes, Different Supply Chain Impact

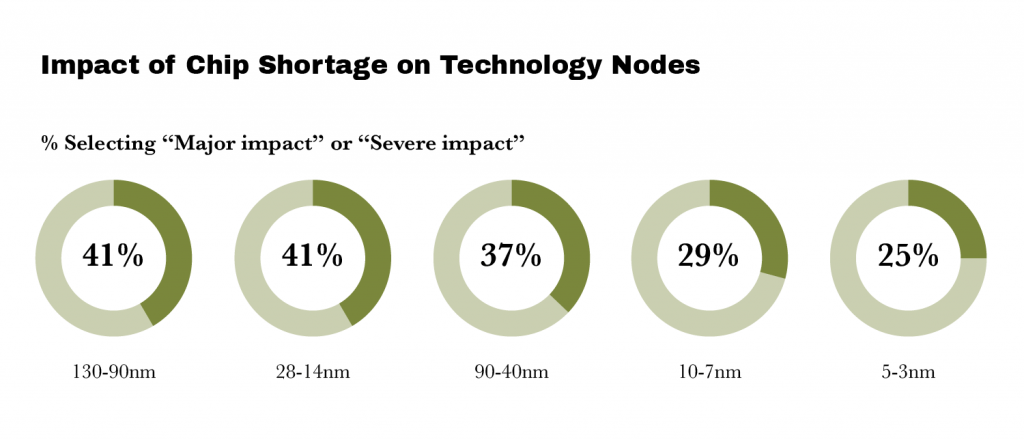

The supply shortage appears not to affect all semiconductor products to the same extent. The more mature nodes are reported to suffer most (with over 4 in 10 respondents indicating the shortage has had a major or severe impact on 130-90nm and 90-40nm nodes), indicating that the mitigation efforts across the industry are mainly focused on the more advanced nodes.

The Future of Semiconductor Industry Growth

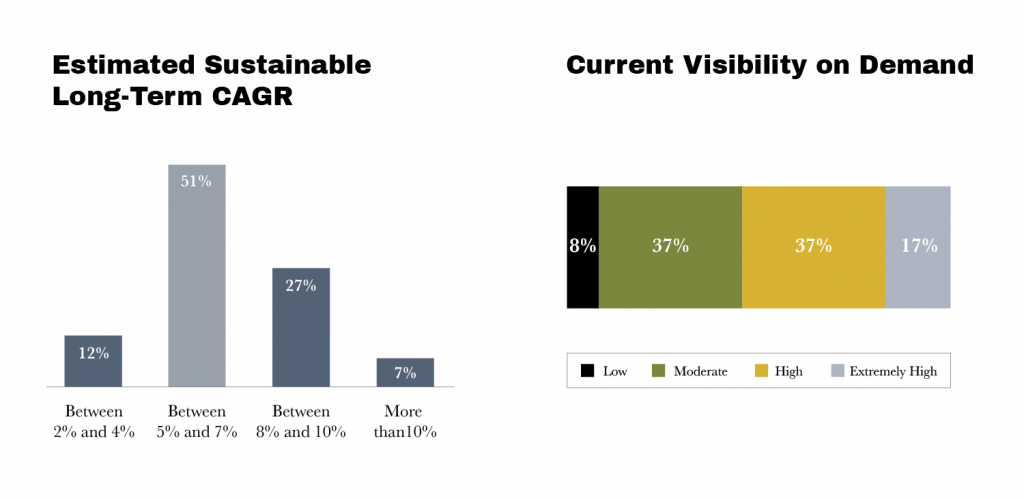

On the longer term, the semiconductor industry is expected to grow at an average compound annual growth rate (CAGR) of 7%. Bear in mind that only 45% of our respondents felt that semiconductor visibility was still at “low” to “moderate” despite recent production capacity corrective actions. The possibility of establishing overcapacity beyond the 2023 horizon is a serious risk that could trigger a major down cycle across the industry.

Reverberations of the Supply Chain Challenges

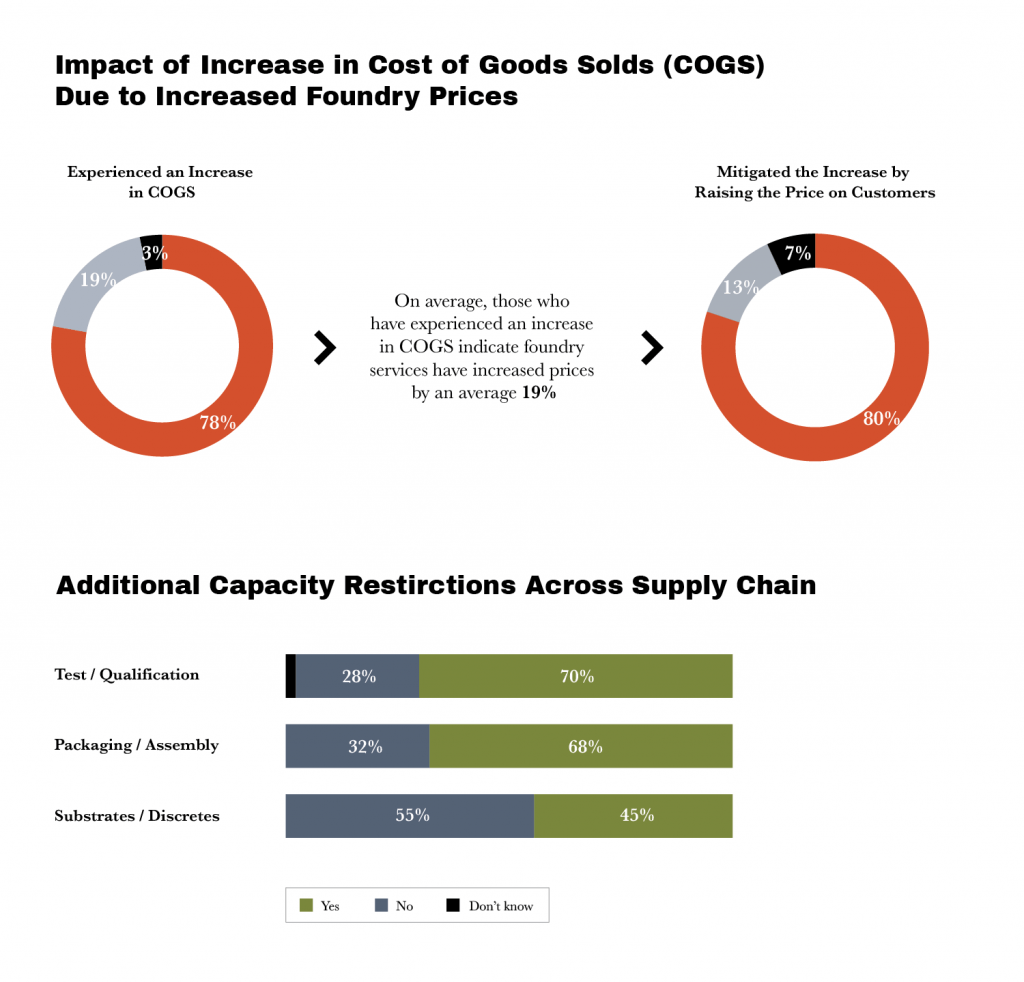

Looking specifically at the impact on businesses, about 8 in 10 respondents indicate their companies have experienced an increase in cost of goods sold (COGS), with an average 19% rise in foundry prices. Among those experiencing increases, 80% mitigated impacts by raising customer prices.

What’s more, experts participating in this survey have also indicated additional capacity restrictions, with 7 in 10 experiencing issues with test/qualification capacity and almost as many with packaging/assembly.

Conclusion

Despite the increasing demand for semiconductors, production of chips suffered due to COVID-19 shutdowns and respondents are experiencing on average an approximately 20% gap in chip demand versus sale fulfillment. Various mitigation actions to face the demand gap have been initiated across the value chain, from expansion of capacity in existing fabless semiconductors to acceleration of plans for building new fabs and from portfolio priority decisions to node migrations for critical parts. Despite these corrective actions, the supply chain gap is expected to last throughout 2023.

Click to Get Access to These Results

or to See Our List of Other Network Surveys

Sample Questions from the Survey:

- What is your outlook for the demand-to-supply volume gap developing in the following periods?

- How would you estimate the split of actual volume demand in terms of inventory (re)build versus actual sell-through?

- Are you facing increases in cost of goods sold (COGS) due to price raises in foundry services (wafers or materials)?

- In your view, how much do the chip shortages impact the following technology nodes?

- Which of the following product classes are most affected by supply shortages?

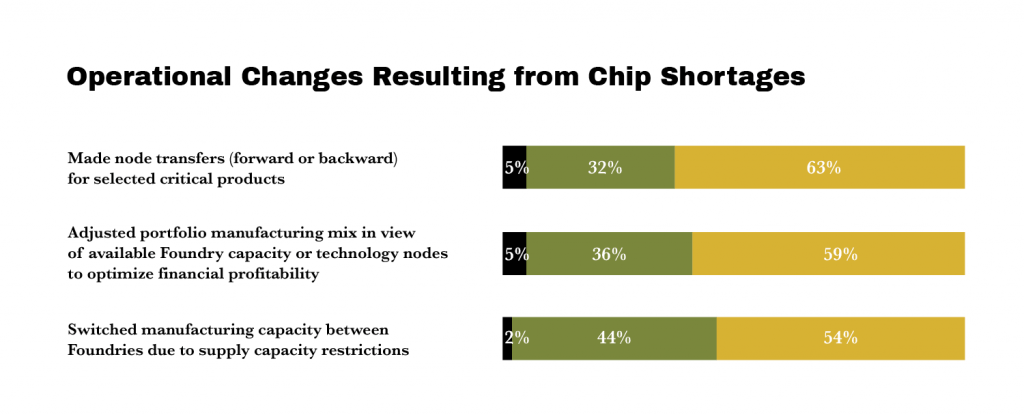

- Have you switched manufacturing capacity between foundries due to supply capacity restrictions?

- Do you anticipate foundries to proactively adjust their global supply chain geographics, i.e., shifting capacity from Asia to EU or USA?

- How are you seeing ASP rising/falling quarter by quarter for semiconductors?

About GLG Network Surveys

GLG’s Network Surveys administer research on market-moving topics and trends, surveying relevant subject matter experts. Each survey focuses on a specific industry, and respondents have in-depth expertise about the latest developments in that industry. To ensure that the survey’s focus is relevant to the panelists, our Network Surveys team partners with a GLG expert with deep industry knowledge to write the questionnaire. GLG currently runs approximately 12 Network Surveys every month.

The standard deliverables for our Network Surveys include:

- 1 x individual responses (“raw data”) in Excel.

- 1 x PPT report with aggregated data.

- For selected topics: executive summary with key takeaways and conclusion.

- For selected topics: in-depth PowerPoint report of survey findings presented by the Network Member via webcast (optional).

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。