Survey: Petrochemical Market Overview

Read Time: 3 Minutes

The impact of the COVID-19 pandemic on the petrochemicals market has been severe, and as a result, the first half of 2021 saw performance fall below expectations across certain segments of this space. However, experts in the field are optimistic that a return to pre-COVID-19 levels is possible by the first half of 2023.

Petrochemical companies are also factoring in climate change and the politics around it, but opinions are split across sectors about the impact it will have on their businesses.

Survey and Panel Demographics

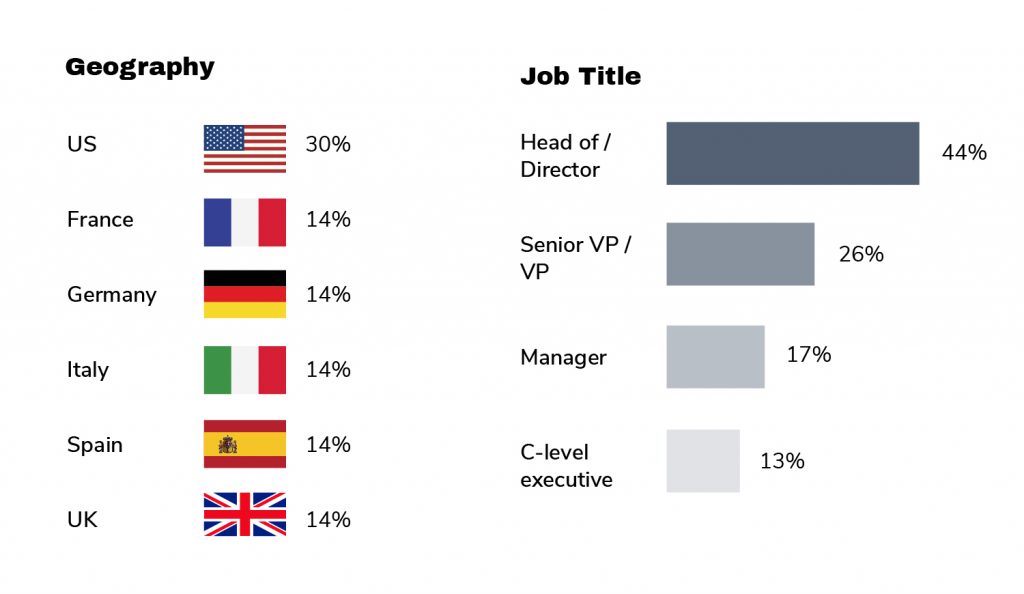

To understand more about the current market dynamics within the petrochemical industry, GLG conducted a survey of 70 senior executives across the U.S. (30%) and Europe (70% in total with an equal split for the United Kingdom, Germany, France, Italy, and Spain). Of those surveyed, 13% were C-suite executives, 17% senior managers, 26% vice presidents, and 44% heads of departments. All our respondents were knowledgeable and able to discuss the latest trends within the petrochemical industry and provided their projections for market recovery.

Petrochemical Market Conditions

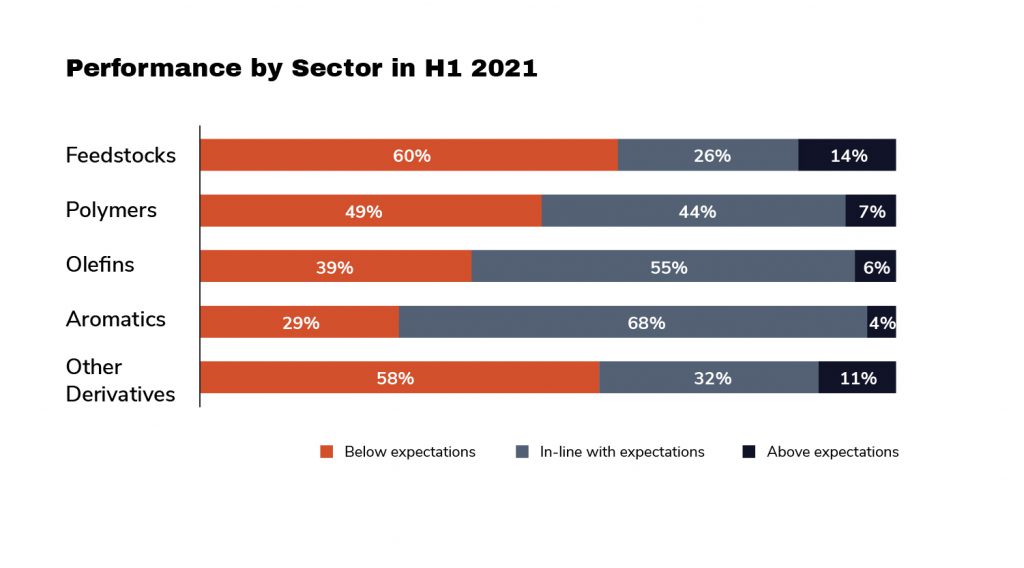

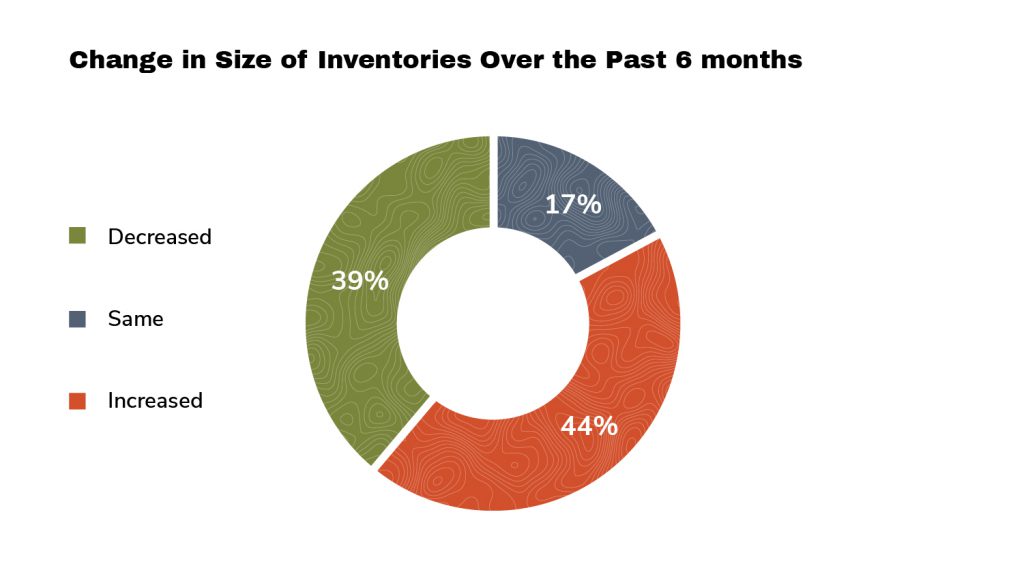

GLG’s survey revealed considerable variation in terms of H1 performance. In the important olefins area, for example, 55% of the respondents reported that H1 2021 performance had been in line with expectations, while 39% saw it as below expectations. A similar divergence was seen upstream: 68% of aromatics respondents saw performance in line with expectations, whereas 60% of feedstocks respondents saw it below expectations. In polymers, the sector closest to end users, 49% saw performance above expectations and 44% saw it below. Perhaps surprisingly in view of the media focus on supply chain problems, 39% said their inventories had increased in H1, twice as many as reported a decrease.

Impact of Climate Change Politics on Petrochemical Industry

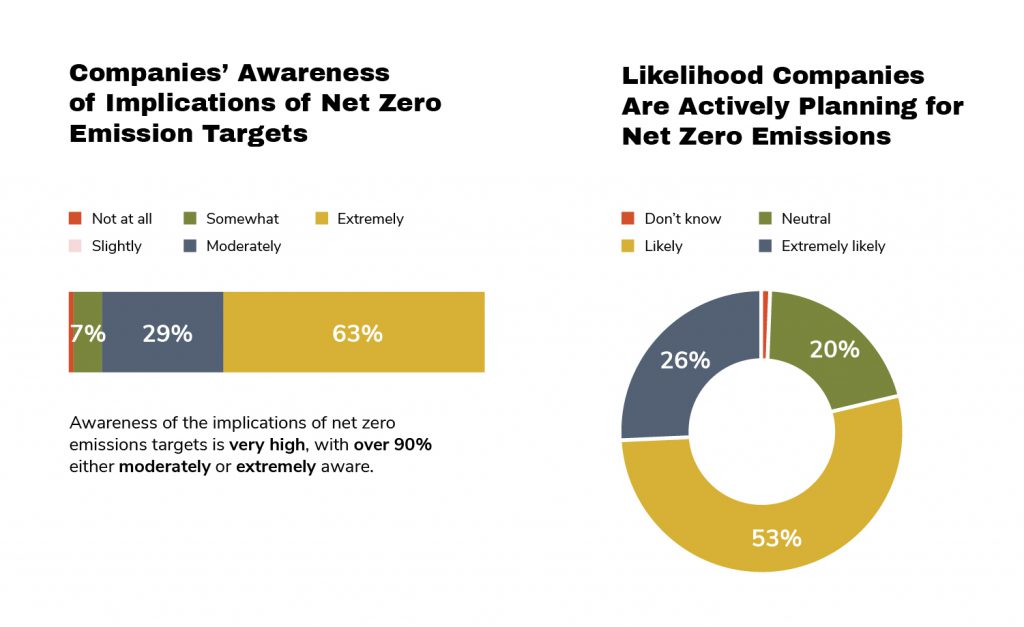

More than 90% of companies are aware of Net Zero emission targets, and half are already planning to meet them. Their expected impact, however, varies by sector. Polymer companies are twice as optimistic about the potential for new opportunities as those in olefins and aromatics. Only a quarter of those involved in feedstocks currently see them as potentially creating new opportunities.

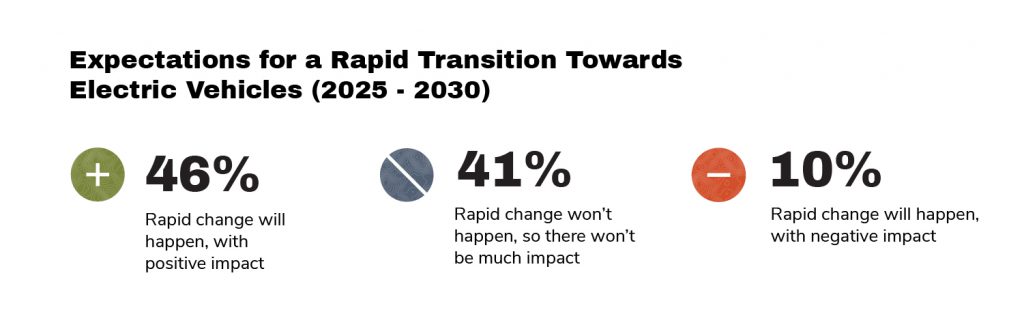

This divergence of views is highlighted in attitudes to the potential for a rapid transition to electric vehicles in the auto sector. Forty-six percent see this as likely to create rapid and positive change, while 41% see little likelihood of this happening — and 10% expect rapid change with a negative outcome for their business.

Conclusion

In the short term, respondents expect the positive momentum established in the first half of 2021 to continue through the end of the year, with those in the aromatics sector most optimistic. Respondents are also positive about the outlook for 2023, led by the polymers sector, where 89% are generally optimistic.

The survey also demonstrated that while petrochemical companies are clearly planning for a Net Zero future, some sectors — like the polymer industry — saw these strictures as presenting opportunities, while others — such as feedstocks — perceive challenges on the road ahead.

Sample Questions from the Survey:

- In your view, what has been the overall COVID-19 impact on the petrochemical market?

- Historically, buyers build inventory when oil prices are rising to protect downstream margins. In your sector, how do you think inventories have been over the past six months?

- How would you describe conditions down the value chain in your main regions?

- In your view, how prepared are companies in your sector in servicing clients in the automotive industry considering the rapid transition from gasoline/diesel cars to electric vehicles?

- What do you think are the biggest challenges when it comes to the transition to autonomous vehicles over the next few years?

- The approaching COP26 conference is likely to see Net Zero emission targets adopted for CO2, with possibly major impact on petrochemicals. Which of the following best apply to your sector?

- Looking further ahead out to 2023, which of the following statements best applies to companies in your region?

- Assuming the oil prices will remain the same, how do you expect your sector to react in H2/2021?

Click to Get Access to These Results

or to See Our List of Other Network Surveys

About GLG Network Surveys

GLG’s Network Surveys administer research on market-moving topics and trends, surveying relevant subject matter experts. Each survey focuses on a specific industry, and respondents have in-depth expertise about the latest developments in that industry. To ensure that the survey’s focus is relevant to the panelists, our Network Surveys team partners with a GLG expert with deep industry knowledge to write the questionnaire. GLG currently runs approximately 12 Network Surveys every month.

The standard deliverables for our Network Surveys include:

- 1 x individual responses (“raw data”) in Excel.

- 1 x PPT report with aggregated data.

- For selected topics: executive summary with key takeaways and conclusion.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。