Survey: Impact of COP26 and Net Zero Strategy

Read Time: 4 Minutes

In general terms, enterprises seem to be aware of the issues surrounding climate change, the need to reduce CO2 emissions, and the need to ensure environmental protection. In the UK, government has laid out a Net Zero Strategy that plans to reduce emissions to net zero in 2050. However, there is mixed knowledge of what the UK Net Zero Strategy means in practice. At the same time, at the recent United Nations Climate Change Conference held in Glasgow (known as COP26), a group of more than 20 governments and financial institutions agreed to stop funding new overseas fossil fuel projects with public money by the end of 2022.

Survey and Panel Demographics

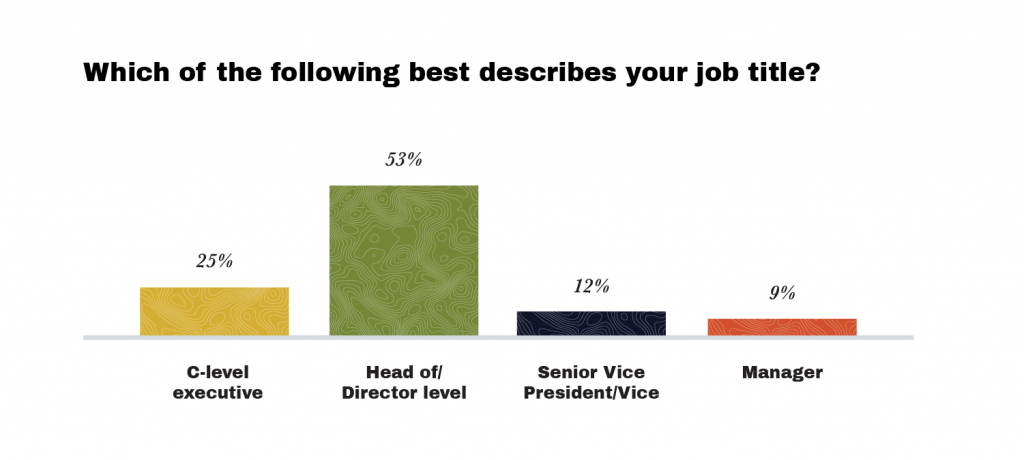

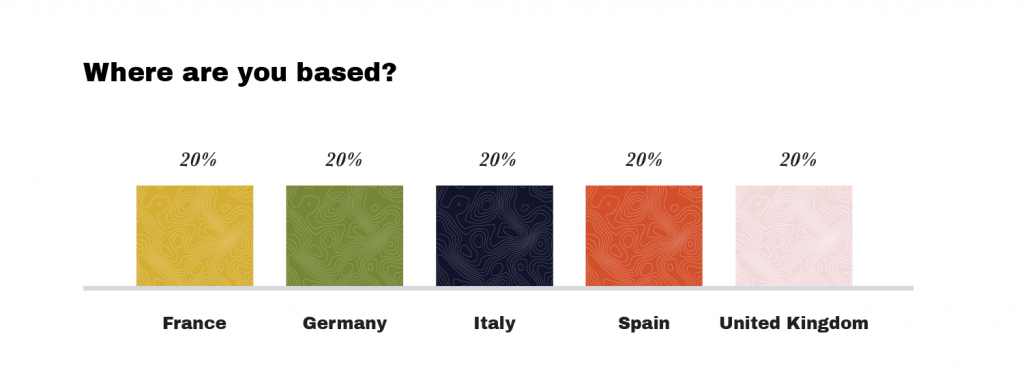

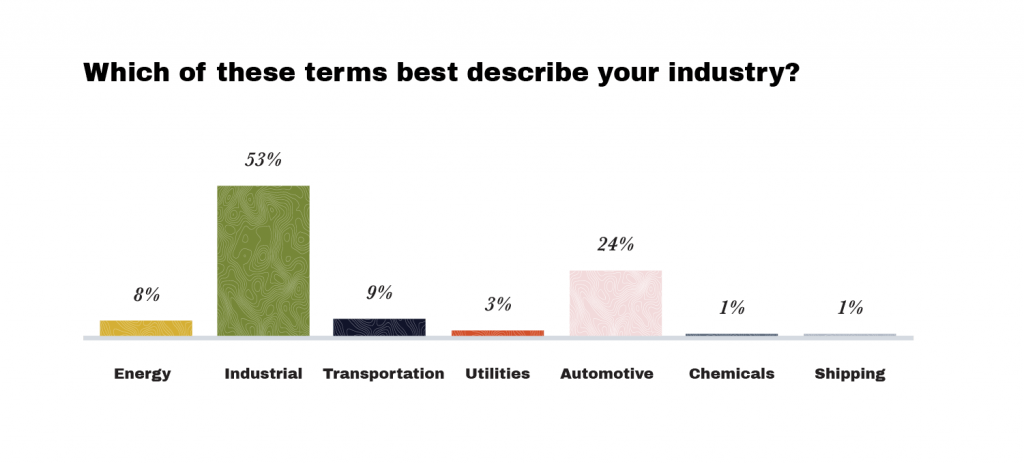

To understand more about this topic, GLG conducted a survey of 75 executives across the UK (20%), France (20%), Italy (20%), Spain (20%), and Germany (20%). Of those surveyed, 53% were head of/director level, 25% were C-suite, 12% senior VP/VP, and 9% manager level. These respondents work in a variety of industries, including industrial (53%), automotive (24%), transportation (9%), energy (8%), utilities (3%), chemicals (1%), and shipping (1%). All respondents were knowledgeable and able to discuss the implications of COP26 and Net Zero on their industry.

Opportunities and Risks

The executives we surveyed perceived climate and environmental issues as both risks (additional costs, unforeseen and unpredictable future, uncertain impact of natural disasters etc.) and a new opportunity for long-term structural (“systemic”) change.

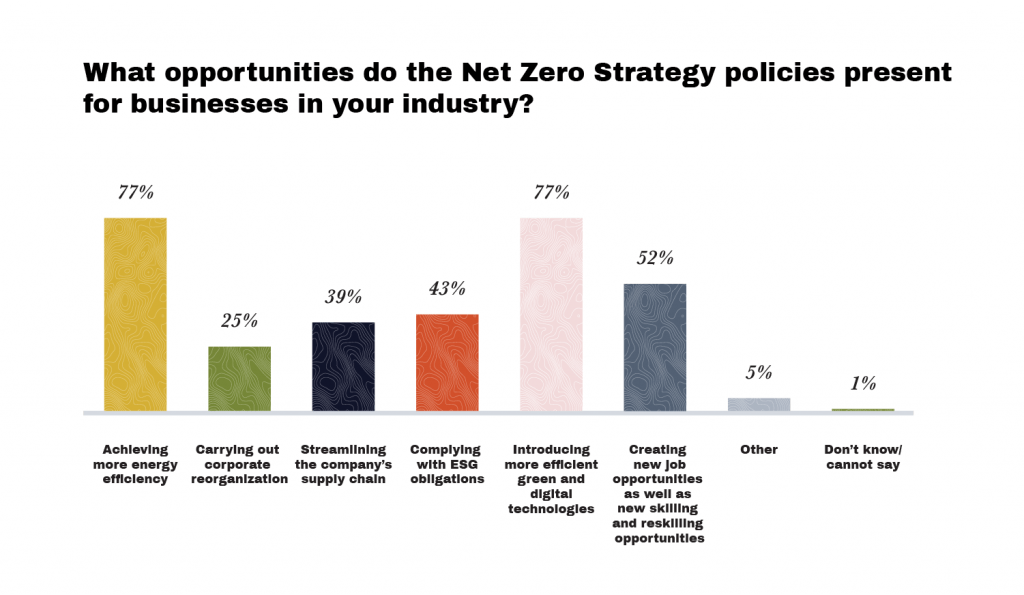

As companies transition toward net zero and COP26, we’ll likely see the introduction of more efficient green and digital technologies, achieving more energy efficiency and shifting from fossil to renewable energy. Three-quarters (77%) of those GLG surveyed support this evolution to non-fossil energy.

Forty-three percent of the executives surveyed named “complying with ESG obligations” as an opportunity, perceiving it as creating a level playing field among enterprises. Other ranked opportunities included “creating new job opportunities” (52%), “streamlining the supply chain” (39%), and “carrying out corporate reorganization” (25%).

Interaction between Enterprises and Government/Public Authorities

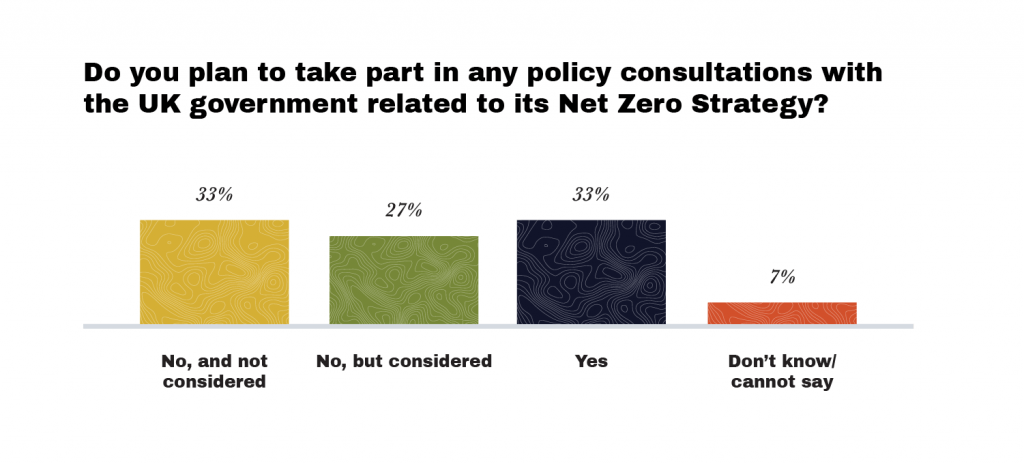

It is uncertain how the interaction between enterprises and government on climate and environmental issues will take place and evolve. Thirty-three percent of the executives we surveyed are of the opinion that there will be no interaction at all between their firm and the public authorities on these matters.

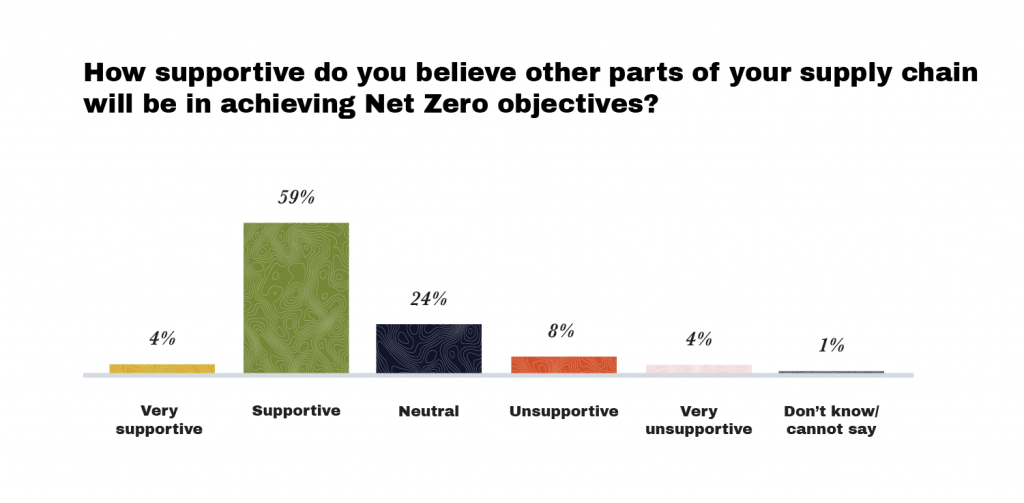

At the same time, enterprises recognize that they will need massive public support in terms of incentives, subsidies, and tax facilitations to support them all through the transition period. Sixty-three percent of enterprises expect a cooperative/supportive position from their global or regional supply chains but 24% estimate that their supply chains will be neutral in this structural decarbonization process to 2050 at European level.

Impact of Extra Costs

Three-quarters of those we surveyed are aware that it is likely or very likely that addressing climate or environmental concerns implies extra costs for them. Transition could be long, expensive, and painful.

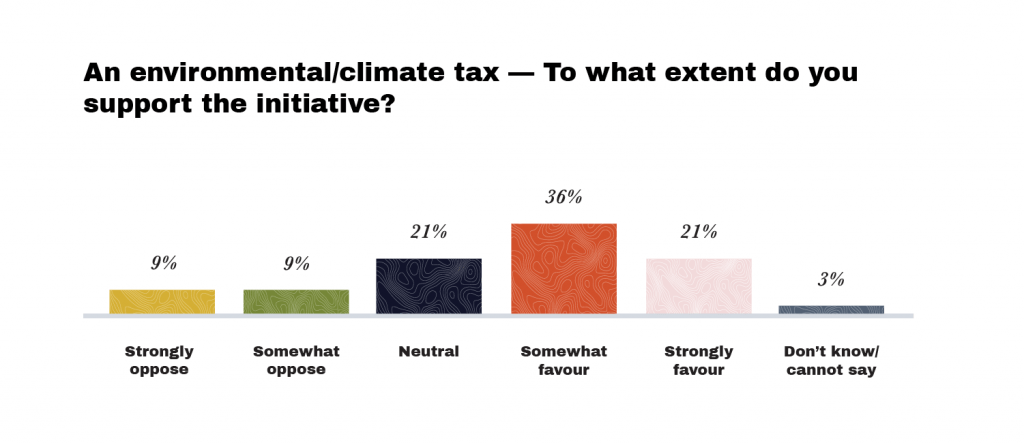

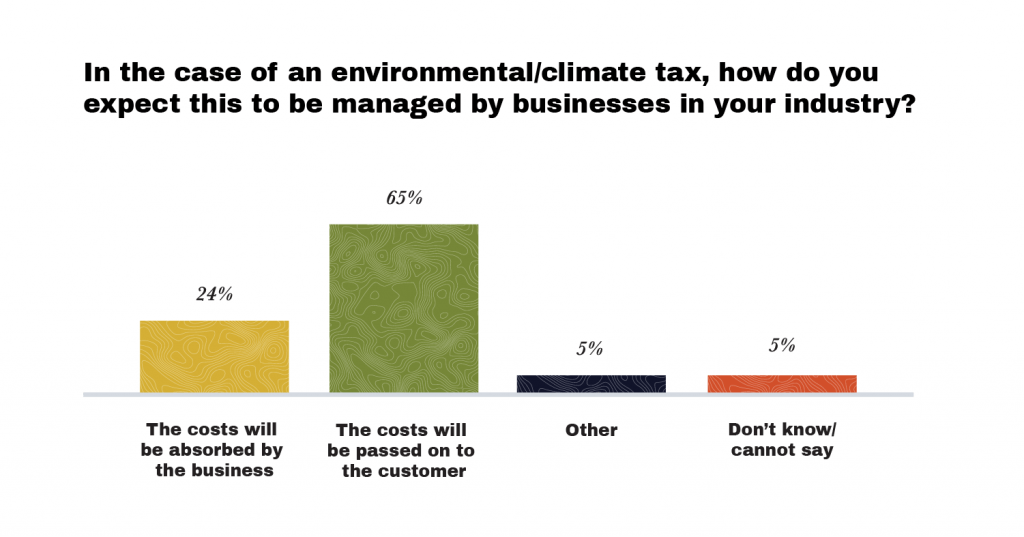

More than 50% of our respondents support a new environmental and climate tax, but 65% of them are ready to pass these extra costs to the clients/consumers. The exact impact of higher costs for consumers is difficult to assess, but for 70% of the enterprises participating in the survey, consumers are “cost sensitive.” This means that passing extra costs to them may bring about declining sales and profits for the enterprises. For them to survive and remain competitive, some of these extra costs would need to be internalized.

CONCLUSIONS

When it comes to net zero and COP26, the executives we surveyed do not underestimate the substantial impact that such a transformation process will have on business models, organization, supply chains, vertical or horizontal integration process, competitiveness, and innovation capacity. They are also aware that this transition process will be long, expensive, and painful. However, they show a degree of resilience and appear rather optimistic. They are ready to seize new business opportunities and invest in innovation, renewable energy, circular economy, environmental protection, digitalization, skilling, and re-skilling.

To achieve the ambitious goals set forth by the Net Zero Strategy and COP26, enterprises will require government incentives and direct financial support. The executives we surveyed demonstrate confidence that public authorities will assist them financially to minimize the social costs of a transition.

Click to Get Access to These Results

or to See Our List of Other Network Surveys

Sample Questions from the Survey:

- To what extent is tackling climate-related issues a priority for your company?

- To what extent do you think businesses within your industry will incur significant costs in the next three years due to climate/environmental concerns?

- To what extent do you expect Net Zero Strategy to impact businesses in your industry?

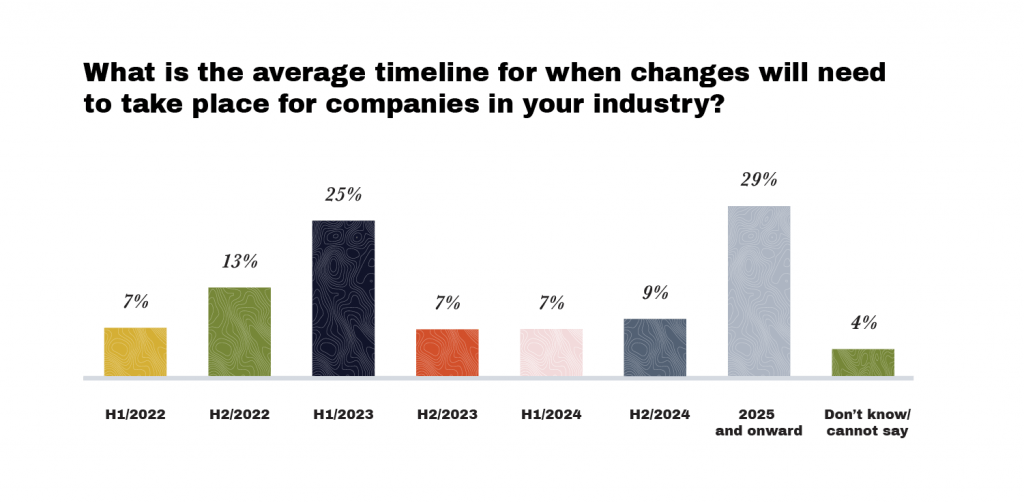

- What is the average timeline for when changes will need to take place for companies in your industry?

- What opportunities do the Net Zero Strategy policies present for businesses in your industry?

- To what extent do you expect the outcomes of the COP26 conference to impact businesses in your industry?

- What will the impact of these changes be on businesses in your industry?

- What opportunities do the outcomes of the COP26 conference present for businesses in your industry?

- Which of the following, if any, will businesses within your industry need to invest in as a result of COP26 objectives?

- In the case of an environmental/climate tax, how do you expect this to be managed by businesses in your industry?

About GLG Network Surveys

GLG’s Network Surveys administer research on market-moving topics and trends, surveying relevant subject matter experts. Each survey focuses on a specific industry, and respondents have in-depth expertise about the latest developments in that industry. To ensure that the survey’s focus is relevant to the panellists, our Network Surveys team partners with a GLG expert with deep industry knowledge to write the questionnaire. GLG currently runs approximately 12 Network Surveys every month.

The standard deliverables for our Network Surveys include:

- 1 x individual responses (“raw data”) in Excel.

- 1 x PPT report with aggregated data.

- For selected topics: executive summary with key takeaways and conclusion.

- For selected topics: in-depth PowerPoint report of survey findings presented by the Network Member via webcast (optional).

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。