Survey: COVID-19 Impact on Airlines and Aircraft Lessors

Read Time: 0 Minutes

The early impact of COVID-19 on airlines was significant. Nonessential air travel was shut down, flights were grounded, and personnel were furloughed. The industry reached its low point in March and April of 2020, and it’s been a slow climb back ever since.

As of August 2021, the airline industry has not yet returned to pre-COVID levels in terms of either active fleets or passenger loads. Now, with the delta variant gaining traction among the unvaccinated population, a challenging road remains ahead for the industry.

Survey and Panel Demographics

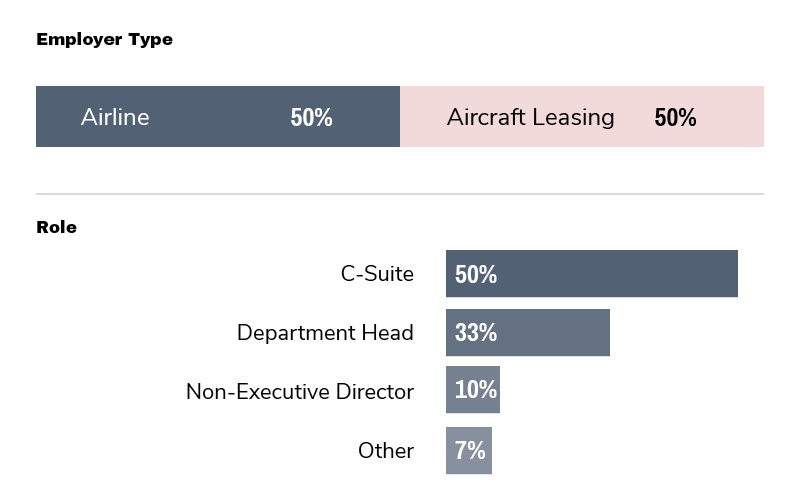

To find out more about the ongoing impact of COVID-19 on the future trends and outlooks for the airline industry, GLG conducted a reoccurring survey of airlines and aircraft lessors across the Americas; Europe, the Middle East, and Africa; and the Asia-Pacific.

To ensure that the survey measured data over time, GLG conducted it in three discrete waves: wave one in September 2020, wave two in March 2021, and wave three in June 2021. Of those surveyed, 50% were C-suite executives and 33% department heads. The remaining 17% were nonexecutives who were either moderately or extremely familiar with their company’s business situation and business decision-making strategy.

Slow COVID-19 Recovery — Airlines

Though social distancing and masking protocols seemed to have some impact on lowering infections since spring 2020’s high point, in September of the same year we were still in the thick of it. On September 27, the World Health Organization said that more than 32.7 million COVID-19 cases had been reported. In that week alone, more than 2 million new cases were reported worldwide.

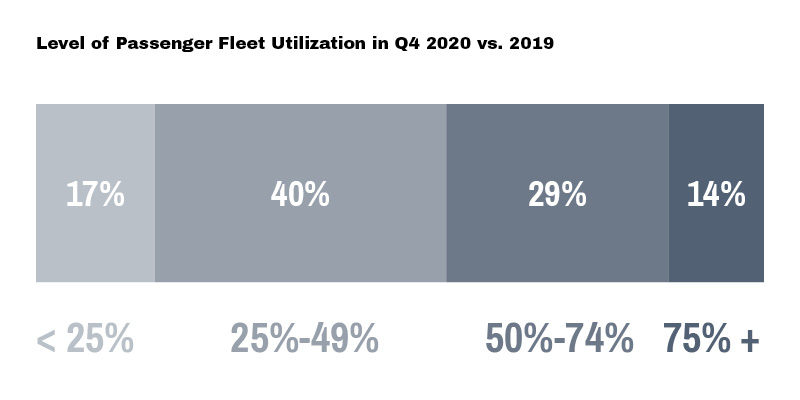

When the first wave of GLG’s survey was conducted in August and September, the airline industry was clearly feeling the stark impact of the pandemic. Almost half of the airline industry professionals whom we surveyed said fleet utilization was less than 25% of 2019 levels, with nearly 85% operating at less than half of pre-COVID-19 levels.

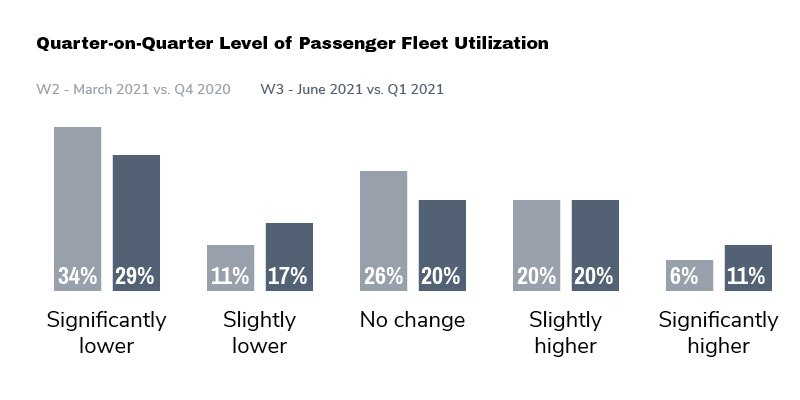

By December 2020, the first vaccines began to roll out. Within the first week, 130,000 were vaccinated in the U.K. and 556,208 received shots in the United States. Since that time, COVID rates have fallen, but airlines are still feeling pain as flight patterns have not yet returned to pre-COVID numbers. The difference between the March and June waves of our survey saw little difference in our respondents’ answers.

When asked about their fleet utilization, nearly 30% of those we surveyed said they continue to see significant decreases and recovery has been reversed in several key markets due to COVID-19 variants and government interventions.

Slow COVID Recovery — Aircraft Lessors

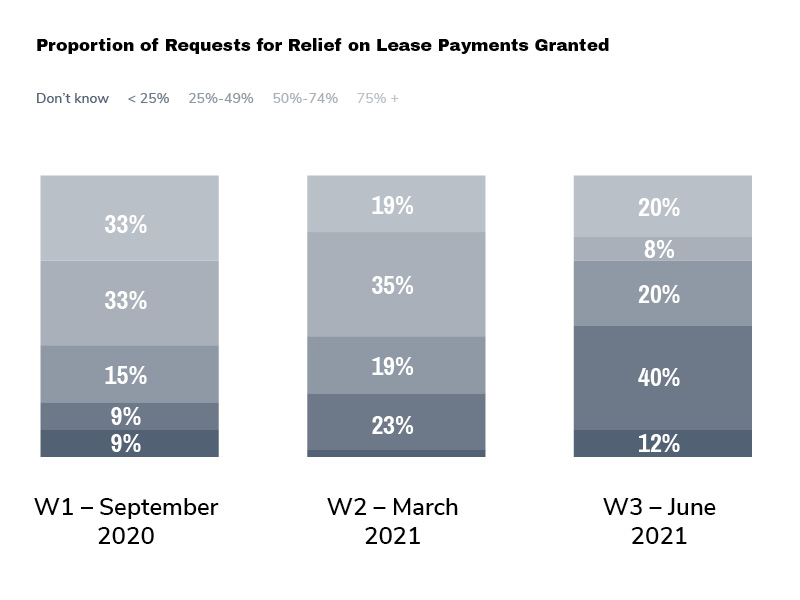

COVID’s impact on airlines rippled through the industry, impacting the aircraft lessors that GLG surveyed. In September 2020, 66% of the lessor respondents said that their companies had granted relief requests. This diminishes to 54% in March 2021 and 28% in June 2021. This still points to a slow recovery for aircraft lessors, which have faced significant income reductions.

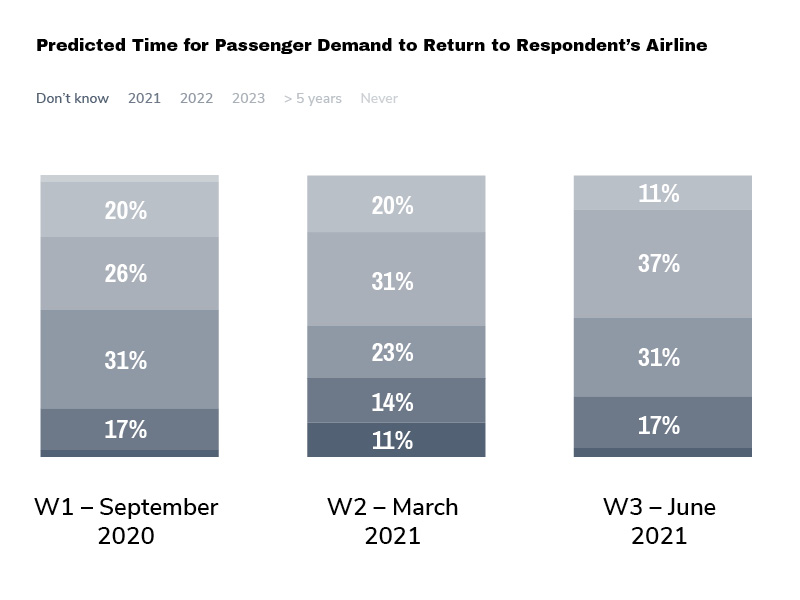

Long-Term Impact of COVID on Airlines and Aircraft Lessors

In September 2020 and March 2021, 20% of our respondents predicted a 2021 recovery. But as COVID persisted, even that optimism waned. In June, just 11% foresaw a complete recovery in 2021. The most widely held view (31% in June) is that a full recovery is not likely until 2023.

Challenges for Airlines and Lessors

GLG’s survey showed that most airline respondents (68%) ranked liquidity as the largest challenge for airlines, with lack of supportive government ranking second (49%). For lessors, the overwhelming concern is now asset value impairment (78%), with oversupply remaining a significant issue (56%).

Conclusion

The world is not out of the COVID woods yet. A critical mass of vaccination is key to sustained recovery. Without that, the delta variant may likely lead us into unpredictable quarantine scenarios that could contribute to an uncertain recovery. But as vaccinations increase, we’ll likely see an early surge in leisure trips and family and friend visits, though business travel and revenue will likely struggle to recover.

Sample Questions from the Survey:

- What is the size of your airline, measured by fleet?

- What percentage is your airline’s approximate fleet mix by body?

- How would you describe your airline’s business model?

- What is the size of your lessor, measured by delivered portfolio?

- What is the approximate portfolio mix by “body”?

- How would you describe your lessor’s investment strategy?

- Compared with 2019, at what level of utilization is the current active passenger fleet operating?

- Compared with your company performance in [previous quarter], what level of utilization is the current active passenger fleet achieving?

- Compared with 2019, what average passenger load factor is currently being achieved?

- Compared with your company performance in [previous quarter], what average passenger load factor is currently being achieved?

- If government support was requested, what conditions, if any, were sought in return?

- What proportion of those requests have been granted in Q1 2021?

- What percentage of lease rental revenue does this represent?

- What is your view on the outlook for the airline industry?

- When do you think passenger demand for your airline will return to 2019 levels?

- Please rank these potential challenges facing airlines in Q2/2021 in order of severity.

- Please rank these potential challenges facing lessors in order of severity.

Click to Get Access to These Results, Watch the Webcast Replay,

or to See Our List of Other Network Surveys

About GLG Network Surveys

GLG’s Network Surveys administer research on market-moving topics and trends, surveying relevant subject matter experts. Each survey focuses on a specific industry, and respondents have in-depth expertise about the latest developments in that industry. To ensure that the survey’s focus is relevant to the panelists, our Network Surveys team partners with a GLG expert with deep industry knowledge to write the questionnaire. GLG currently runs approximately 12 Network Surveys every month.

The standard deliverables for our Network Surveys include:

- 1 x individual responses (“raw data”) in Excel.

- 1 x PPT report with aggregated data.

- For selected topics: executive summary with key takeaways and conclusion.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。