2020 Has Been Hijacked by COVID-19: How Are Banking and Payments Changing as a Result?

Read Time: 0 Minutes

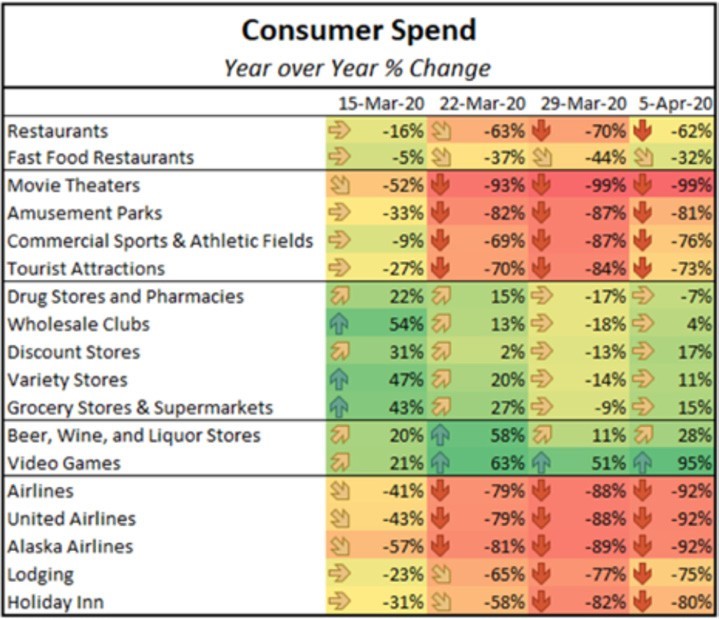

With shelter-in-place and social distancing mandates presiding in most parts of the country, we’ve seen devastating decreases in consumer spending at most businesses (with the understandable exceptions of groceries and liquor stores) and dramatic shifts in consumer behaviors and preferences, away from in-person purchases and toward order ahead, delivery, and cashless payments.

Businesses are finding or focusing on new ways of accepting payments when all business has gone either virtual or minimal contact. The World Health Organization (WHO) has discouraged using cash, indicating it can be a carrier for the virus. The WHO instead encourages the use of contactless payment technology. Many stores have stopped accepting cash, some to the point of having the consumer read their card number aloud instead of handing it to the cashier.

Inevitably, the overall decline in spending because of stay-at-home orders is impacting payments companies significantly. Visa saw March spending by U.S. cardholders drop by 4%, and overseas spending dropped by 19%; these numbers will worsen in April and probably beyond. As a result, PayPal, Mastercard, Visa, and others have revised 2020 revenue estimates downward and will continue to do so as the impacts of the pandemic are revealed in the coming months.

Retail, Restaurants, and Delivery

Restaurants closed for dine-in service have favored using delivery services like Uber Eats, Grubhub, and DoorDash. This allows restaurants to continue earning revenues and employing at least a portion of their staff.

Food delivery was already a rapidly growing sector, but the current crisis is forcing more restaurants to align with those services, or develop their own remote ordering and delivery service, to keep the lights on and save on steep delivery service commissions. Many restaurants have also set up curbside pickup options to protect their margins and now take payment information over the phone at the time of the order so pickup is a contactless transaction.

Many retail establishments closed to foot traffic are now offering curbside pickup, shifting to more online shopping, and providing free local delivery. An independent children’s bookshop in my town set up a little bookcase outside its front door; customers provide an estimated pickup time when they order, and the shop employees place the completed order and receipt on the bookshelf before pickup time and disappear back inside: the COVID-19 twist on the Buy Online Pickup in Store trend of the last few years.

Banking Redefined

Banking activity has also shifted dramatically, with most branches now offering drive-thru service and meetings by appointment only (if at all). This has driven more consumers and businesses to the online and mobile channels, with a recent survey showing two-thirds or more of consumers are more likely to try digital banking options.

Most bank websites are highlighting their online and mobile offerings on their homepages, reminding customers that 24/7 access is available. On its homepage, American Express states, “Our customer care teams are hard at work to help you, but wait times are higher than normal. We strongly encourage you to use our digital tools for self-servicing. You can access your accounts online and by using the Amex App.” Similar messages can be found at TD Bank, SunTrust, KeyBank, and many others.

How Financial Services Players Are Supporting Impacted Customers

It’s important to note not just how payments are being made in these new times but also of payments that will NOT be made. Furloughed and laid-off workers will have difficulty making their payments for rent, mortgage, credit cards, and more.

Some larger banks, like Wells Fargo, JPMorgan Chase, and Bank of America, have indicated they will extend payment deadlines, waive late fees, and even suspend loan payments for up to three months, along with not reporting missed payments to credit bureaus. Apple is letting Apple Card users defer March and April payments without incurring interest.

Some payments and fintech companies are also finding ways to help small businesses manage through the downturn. Square is waiving software subscription fees for many of its services, including Square for Restaurants, Square for Retail, and Square Payroll services. It’s also promoting online store setup, options for limiting in-person contact (e.g., signature waivers), and the enablement of digital gift cards.

Several delivery companies, including DoorDash, Postmates, and Grubhub, are waiving or deferring commission fees for independent restaurant partners; however, many industry players contend that the delivery companies are doing too little and profiting while their restaurant clients are being driven out of business. An excellent and frequently updated list of fintech firms providing free technology to banks and others during the coronavirus crisis can be found here.

What Industry Players Can Do Now

Beyond offering special programs to help consumers and businesses negatively impacted by coronavirus, key stakeholders should focus on preparing for these enduring changes in customer behavior:

- Financial Institutions, Payments Service Providers, and Delivery Services Providers: Leverage this time to strengthen digital capabilities by simplifying customer interfaces, enhancing product offerings, and exploring partnership possibilities.

- Restaurants/Retail: Build infrastructure or partnerships to support the longer-term shift of a portion of the business to online/mobile ordering, delivery, and pickup.

- Consumer Goods: Explore which digital banking, ordering, and delivery services are most crucial and provide the best customer experience during this difficult time.

The steps that industry players take now to adapt and support their customers are critical to earning or retaining loyalty once we’re on the other side of this crisis.

About Ginger Schmeltzer

Ginger Schmeltzer is Owner and Principal at GDS Advisors, LLC. Previously, she was Senior Vice President of Emerging Payments at Fiserv, Inc., where she led development and execution of enterprise-wide initiatives to facilitate the delivery of new payment services. Prior to this, she served as Senior Vice President of Digital Channel Management at SunTrust Bank, where she oversaw online banking, mobile banking, and digital money movement technologies, in addition to online sales and the SunTrust.com website.

GLG Projects deliver you strategic recommendations informed by real-world expertise. Learn more.

订阅 GLG 洞见趋势月度专栏

输入您的电子邮件,接收我们的月度通讯,获取来自全球约 100 万名 GLG 专家团成员的专业洞见。